Marina Lubimova

Marina Lubimova

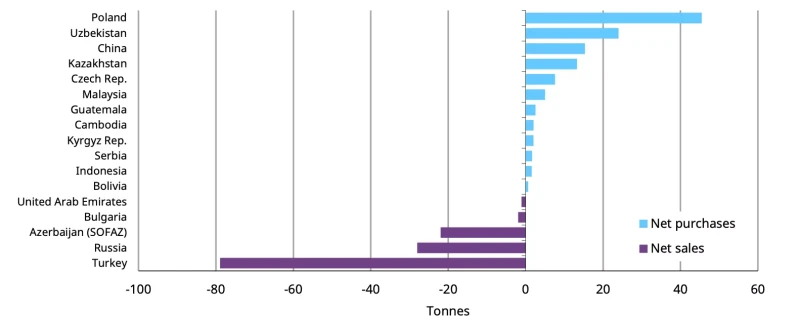

The headline number is relatively modest. The buyer list is not. Poland, Uzbekistan, China, Kazakhstan and the Czech Republic were among the largest purchasers. Turkey, Russia and Azerbaijan's sovereign wealth fund were sellers.

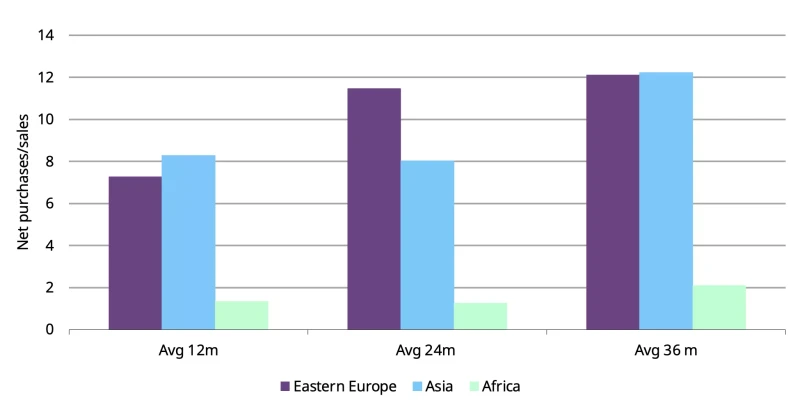

That split says more about the gold market than the 17-tonne figure itself. The most active buyers are no longer concentrated in the world's traditional financial centers. They are increasingly located in Eastern Europe and Asia - regions facing a different mix of geopolitical, monetary and economic pressures than their Western counterparts.

Poland has become the clearest example of this shift. The country's central bank added another 49 tonnes in April, extending a buying program that has transformed it into one of the largest official-sector gold purchasers in the world. Uzbekistan added more than 20 tonnes, while China continued steadily increasing its reserves.

These are not opportunistic trades. They are part of multi-year reserve strategies that have continued through rising interest rates, a stronger dollar and record-high gold prices.

Poland, Uzbekistan and China led April's purchases, while Turkey remained the largest seller.

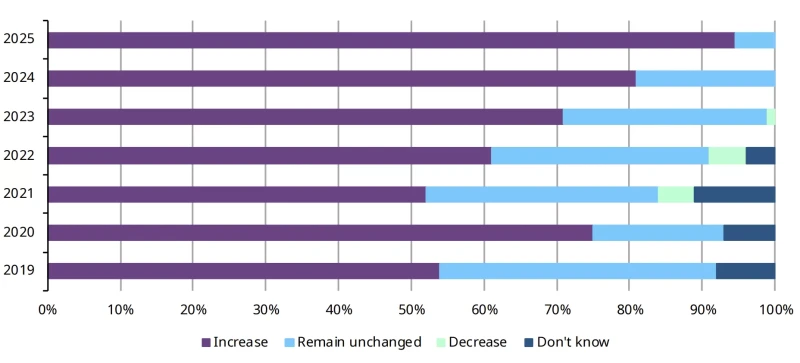

The pattern extends well beyond a single month. According to the World Gold Council's latest survey, most central banks expect global gold reserves to either increase or remain unchanged over the next 12 months. Virtually none expect official holdings to decline.

Even institutions that are not actively buying show little appetite for reducing exposure.

Central banks overwhelmingly expect global gold reserves to rise or remain stable. That would have been a surprising result a decade ago. Reserve management was still largely a dollar story. Gold remained important, but mostly as a legacy asset inherited from previous monetary eras.

Today, the role of bullion is changing. For many reserve managers, gold is one of the few assets that sits outside another country's political and monetary system. It carries no issuer risk and requires no confidence in a foreign government's fiscal position.

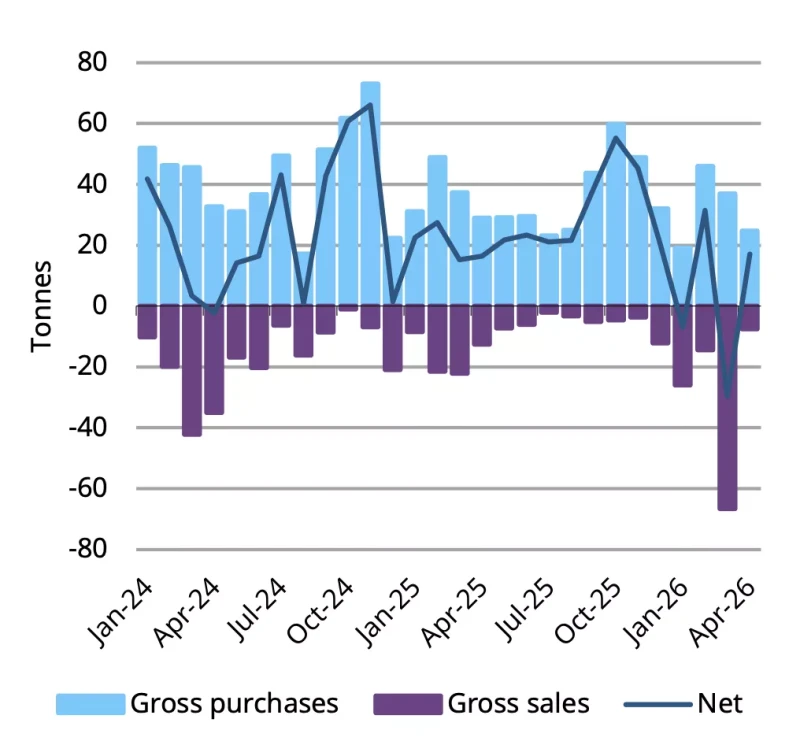

Chart 2. Eastern Europe and Asia have dominated net central-bank gold purchases over the past three years. March briefly interrupted that narrative. Official-sector sales exceeded purchases, prompting speculation that central banks were becoming less willing to buy gold near record highs.

April restored the trend. Net purchases returned, suggesting that March was less a strategic reversal than a period of profit-taking and portfolio rebalancing.

March's selling wave stands out as an exception within a broader buying trend.

Central banks appear to be looking at something else. The countries driving official demand are not chasing momentum. They are building reserves for a world that looks increasingly fragmented and less dependent on a single financial center.

March created doubts. April showed those doubts may have been premature. The world's biggest financial hubs are no longer driving central-bank gold demand. The momentum is coming from Eastern Europe and Asia, where reserve managers appear far more focused on resilience than yield. For years, investors treated gold as a hedge against uncertainty. Increasingly, central banks are treating it as infrastructure.

Marina Lubimova

Marina Lubimova