Artem Voloskovets

Artem Voloskovets

Forecasts of the dollar's decline have followed almost every geopolitical shock, financial crisis, or BRICS summit. Yet the latest IMF reserve data tells a far less dramatic and ultimately more important story.

The dollar is not being replaced. It is being diluted. Central banks are steadily reducing exposure to a single reserve currency, not because another has emerged as a credible successor, but because today's geopolitical landscape rewards diversification. The result is a quieter transformation: the reserve system is becoming broader rather than simply shifting from one dominant currency to another.

One Direction, Twenty-Five Years

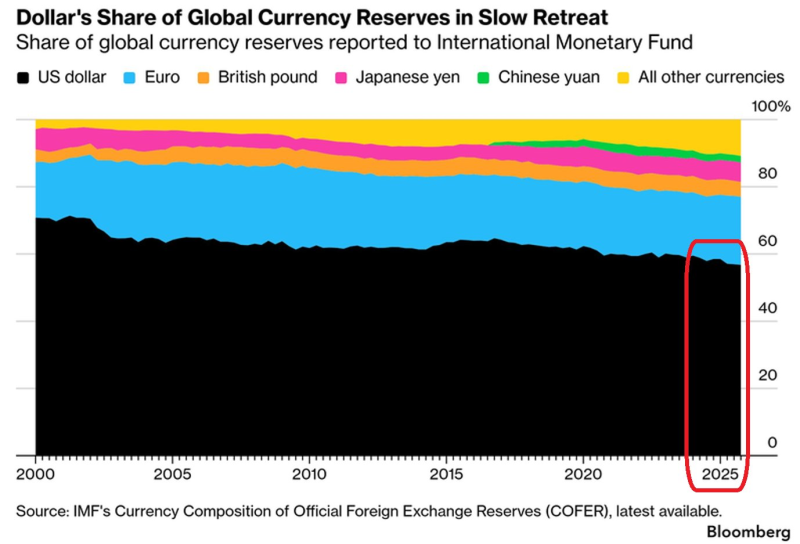

The long-term trend leaves little room for debate. Around the turn of the century, nearly seven dollars out of every ten held in official foreign exchange reserves were denominated in U.S. currency. By the end of 2025, that figure had fallen to 56.77%.

Measured over twenty-five years, the decline appears substantial. Measured quarter by quarter, however, it is almost imperceptible. This is not how reserve currencies lose credibility. It is how portfolio preferences evolve.

Liquidity remains overwhelmingly concentrated in U.S. financial markets, and no competing currency offers comparable depth or global acceptance. What has changed is not confidence in the dollar itself, but the willingness of central banks to rely so heavily on a single asset.

The Real Shift Is Happening Elsewhere

Much of the public discussion assumes that every percentage point lost by the dollar automatically strengthens China's renminbi. The data points in another direction.

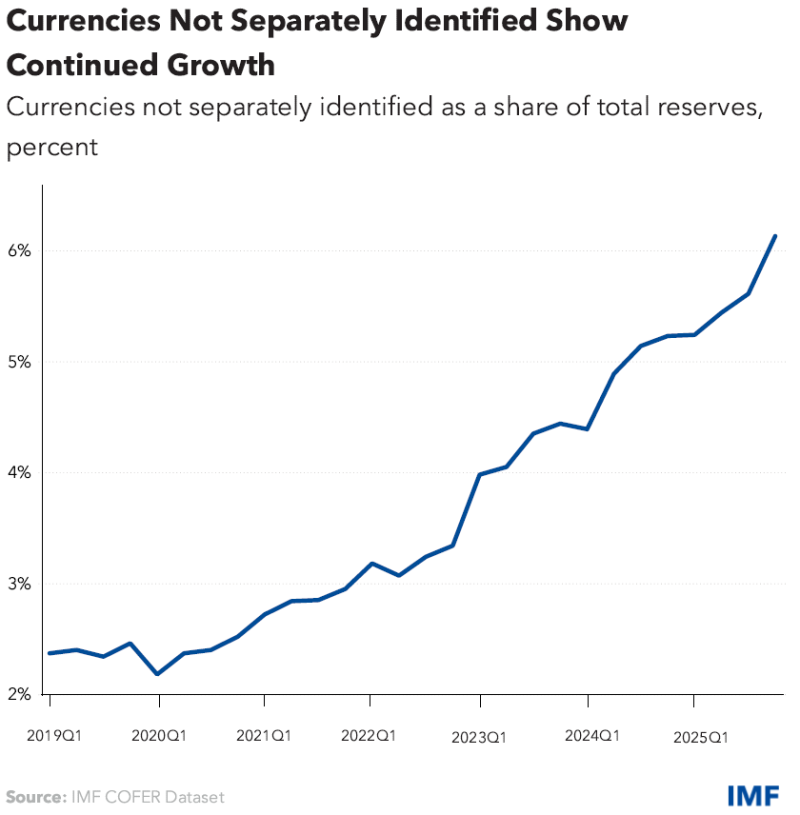

The renminbi accounted for 1.95% of allocated reserves in the fourth quarter of 2025, almost unchanged from recent years. The standout performer is instead the category labeled "Other currencies."

Its share has climbed from roughly 2.3% in 2019 to 6.13% today. That increase says more about reserve management than about any individual currency. Rather than concentrating new allocations in one alternative, central banks are distributing capital across a growing range of reserve assets, from Australian and Canadian dollars to Scandinavian currencies and other regional markets. The destination is not a new monetary leader.

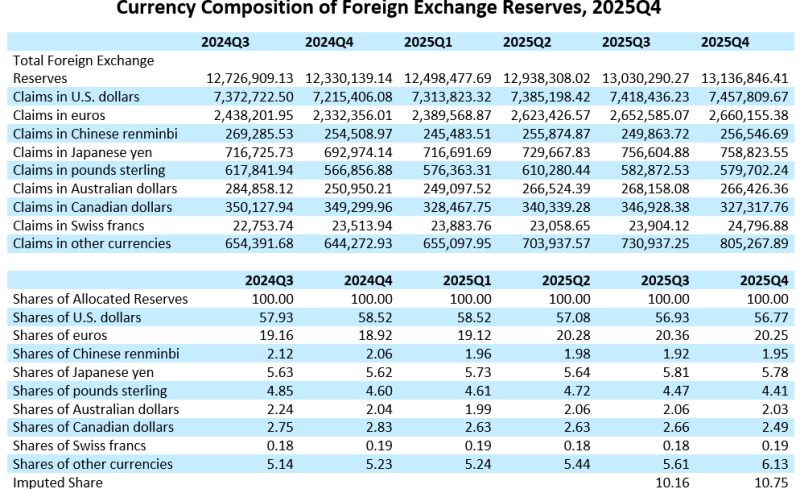

The fourth-quarter numbers expose one of the most misunderstood aspects of reserve statistics. Global foreign exchange reserves expanded from $13.03 trillion to $13.14 trillion. Dollar holdings also increased, rising from $7.42 trillion to $7.46 trillion. Yet the dollar's share slipped again, from 56.93% to 56.77%. There is no contradiction. Reserve shares measure relative weight, not absolute demand. The world is holding more dollars than before. It is simply accumulating other reserve currencies at a faster pace. That distinction changes the entire interpretation of the data.

Insurance Against Uncertainty

Reserve management today looks very different from what it did twenty years ago. Liquidity is no longer the only objective. Political fragmentation, financial sanctions, regional payment systems, and shifting trade relationships have introduced a second priority: resilience. From that perspective, holding a broader mix of reserve currencies is less a judgment on the United States than a response to a more uncertain operating environment. Diversification has become a form of insurance.

Scale Still Matters

None of this alters the structural advantages that continue to support the dollar. The U.S. Treasury market remains the world's largest pool of risk-free collateral. Dollar funding underpins international banking. Commodities continue to be priced primarily in dollars, while global payment and settlement systems still revolve around U.S. currency. Reserve allocations have become more diversified. Financial infrastructure has not. That distinction explains why the dollar can lose market share without losing its central role.

Beyond Foreign Exchange

Foreign exchange reserves represent only one side of the balance sheet. Gold has quietly become another major destination for official reserve accumulation. Unlike sovereign currencies, bullion carries neither issuer risk nor political jurisdiction. For central banks seeking greater strategic flexibility, it complements rather than replaces traditional reserve assets. Viewed together, the rise of gold and smaller reserve currencies points to the same conclusion. The objective is no longer maximum exposure to the world's largest reserve currency. It is maximum flexibility under an increasingly fragmented global order.

A Different Kind of Transition

The search for the currency that will replace the dollar has dominated financial commentary for years. The latest IMF data suggests that the question itself may be outdated. No single challenger is absorbing the dollar's declining share. Instead, reserve managers are building portfolios that assume the future will be less predictable, more regional, and politically more complex than the past. The dollar remains the cornerstone of the international monetary system. What is disappearing is something else: the expectation that one currency should dominate to the extent it once did.

Artem Voloskovets

Artem Voloskovets