Marina Lubimova

Marina Lubimova

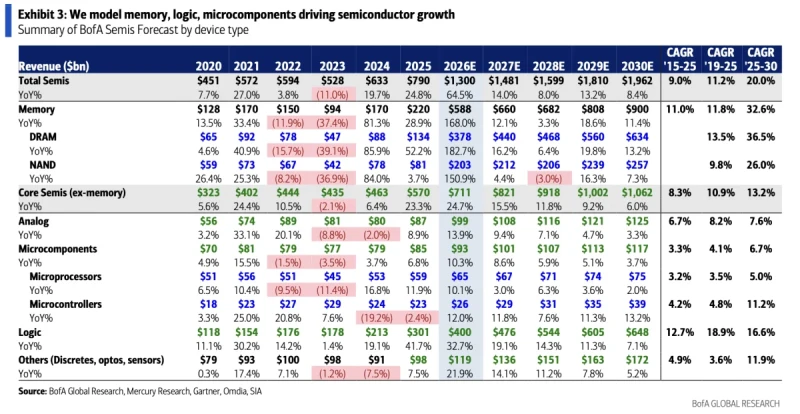

The market is no longer driven primarily by smartphones, PCs, or traditional server deployments. AI data centers are becoming the dominant source of incremental demand, pulling capital into processors, memory, networking, packaging, and power infrastructure simultaneously. BofA expects semiconductor revenue to almost triple by the end of the decade.

| Year | Revenue |

| 2024 | $633B |

| 2025 | $790B |

| 2026 | $1.30T |

| 2027 | $1.48T |

| 2028 | $1.60T |

| 2029 | $1.81T |

| 2030 | $1.96T |

The sharpest acceleration appears in 2026, when industry revenue is projected to increase by 64.5% year-over-year. Such growth would be unprecedented for a sector that historically expanded through cyclical demand from consumer electronics and enterprise hardware.

Memory Is Growing Faster Than The Rest Of The Industry

The most significant detail in BofA's forecast is not the headline market size but the composition of future growth. Memory revenue is projected to rise from $220 billion in 2025 to $900 billion by 2030. During the same period, the rest of the semiconductor industry grows from $570 billion to $1.06 trillion.

| Segment | 2025 | 2030 |

| Memory | $220B | $900B |

| Core Semiconductors | $570B | $1.06T |

The gap in growth rates is even more revealing.

- Memory CAGR (2025–2030): 32.6%

- Total Semiconductor CAGR (2025–2030): 20.0%

- Core Semiconductor CAGR (2025–2030): 13.2%

Memory accounts for a disproportionate share of industry expansion over the next five years, suggesting that AI infrastructure is becoming increasingly constrained by data movement rather than raw compute capacity.

AI Workloads Are Reshaping Demand For Memory

Large language models require constant movement of vast amounts of data between processors and memory. As model sizes increase, memory bandwidth becomes a limiting factor. Additional compute capacity delivers diminishing returns when processors spend time waiting for data. This dynamic has transformed high-bandwidth memory from a specialized component into one of the most important technologies in modern computing.

BofA expects DRAM revenue to rise from $134 billion in 2025 to $634 billion by 2030.

The forecast implies that DRAM alone will generate roughly half a trillion dollars of additional annual revenue by the end of the decade. Few segments in the technology industry have ever expanded at that scale.

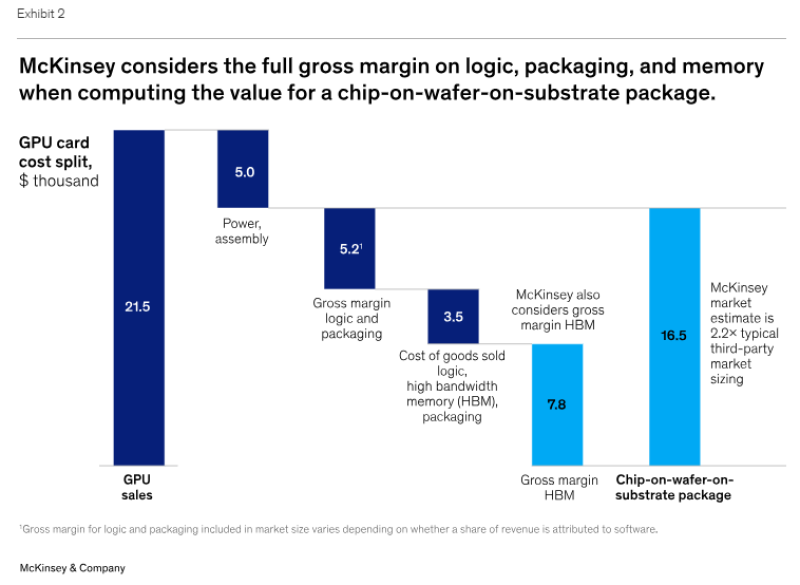

The Industry Is Creating Value Beyond The Chip

Another reason behind BofA's larger TAM estimate is the growing importance of technologies that sit around the processor rather than inside it.

Advanced packaging, high-bandwidth memory, interconnect technologies, and system-level integration account for an increasing share of performance improvements in AI hardware.

Research from McKinsey argues that traditional semiconductor market measurements fail to capture a meaningful portion of this value creation because they focus on individual chips rather than complete computing systems.

Use McKinsey GPU package valuation chart. This distinction becomes increasingly important as AI accelerators evolve into tightly integrated platforms that combine compute, memory, packaging, and networking within a single architecture. The result is a growing gap between semiconductor revenue and the broader economic value generated by AI infrastructure.

What The $2.7 Trillion Forecast Actually Signals

The semiconductor industry's expansion is no longer a simple story of faster processors and higher chip volumes. The fastest-growing parts of the market are increasingly tied to memory, packaging, and system integration. These technologies receive far less attention than GPUs, yet they are becoming essential to scaling modern AI systems.

BofA's revised forecast reflects this transition. The industry is moving away from a processor-centric model toward a platform-centric model in which performance depends on the efficiency of the entire system. That shift helps explain why semiconductor growth is accelerating and why estimates for the industry's long-term opportunity continue to move higher.

Marina Lubimova

Marina Lubimova