Marina Lubimova

Marina Lubimova

The revision follows a quarter in which Apple delivered record revenue, expanding margins and another wave of shareholder returns, giving analysts stronger reasons to raise their valuation.

The new target suggests Wall Street sees Apple's value resting on several durable businesses, premium hardware, a rapidly expanding Services segment and exceptional cash generation, rather than a single AI catalyst.

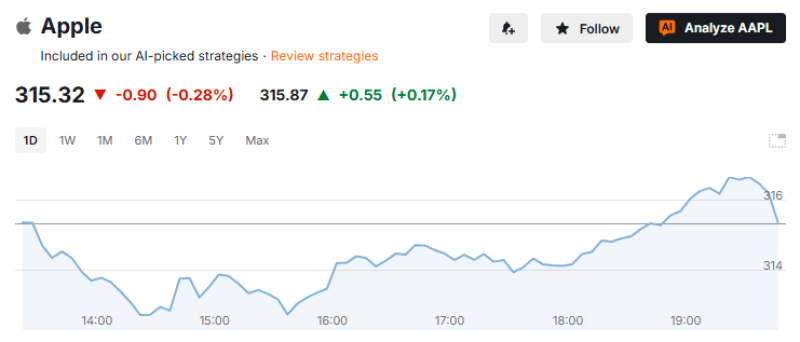

Apple shares traded around $315 throughout the session, briefly moving above $316 before easing back toward the close. The limited price reaction indicates that investors viewed Citi's higher target as supportive, while waiting for future product announcements and earnings to justify a materially higher valuation.

Strong Financial Results Are Driving the Re-rating

Apple's latest quarterly report provides much of the evidence behind a more optimistic outlook.

For the fiscal second quarter ended March 28, the company reported:

- Revenue of $111.2 billion, up 17% year over year

- Diluted EPS of $2.01, an increase of 22%

- Record Services revenue of $31 billion

- More than $28 billion in operating cash flow

- A 4% increase in the quarterly dividend

- Authorization for an additional $100 billion share repurchase program

Record iPhone revenue, continued growth in Services, and strong demand for newly introduced iPads and Macs pushed the company to its best-ever March quarter. Those results strengthen the case that Apple's earnings momentum remains intact despite its enormous scale.

AI Is Part of the Story, Not the Entire Thesis

Much of the market has spent the past several months trying to determine whether Apple can become a leading AI company.

Citi's view is broader. The firm's research argues that Apple's investment case should not depend exclusively on AI announcements. Instead, the company benefits from several reinforcing advantages: a loyal installed base, recurring subscription revenue, premium pricing, and one of the strongest balance sheets in the technology sector.

Artificial intelligence may encourage future hardware upgrades, but it is only one component of a business that is already generating record profits.

Services Continue to Increase Their Importance

The Services division has become one of Apple's most valuable assets. Quarterly Services revenue reached a record $31 billion, reflecting continued growth across subscriptions, digital payments, cloud storage, and the App Store ecosystem.

Unlike hardware sales, these businesses generate recurring income and typically deliver higher operating margins. As Apple's installed base continues to expand, Services provide an increasingly stable source of earnings regardless of annual device replacement cycles.

That consistency has become an important factor supporting higher valuation multiples.

Cash Flow Gives Apple Multiple Options

Apple generated more than $28 billion in operating cash flow during the quarter while simultaneously increasing its dividend and approving another $100 billion buyback program.

The scale of that cash generation gives management considerable flexibility. Apple can continue investing in AI, fund new hardware development, expand shareholder returns, and preserve one of the strongest balance sheets in the industry without placing pressure on its finances.

A Higher Target Comes With Higher Expectations

A price target of $365 assumes Apple can continue producing exceptional financial results. Future earnings reports will need to show that Services maintain their momentum, hardware demand remains resilient and AI features translate into measurable commercial benefits rather than simply attracting attention.

The higher valuation therefore reflects confidence in Apple's execution as much as confidence in its technology roadmap. If the company continues to combine steady earnings growth, disciplined capital allocation and successful product launches, Citi's revised target could prove achievable.

Marina Lubimova

Marina Lubimova