Artem Voloskovets

Artem Voloskovets

- The national average understates the regional strain

- A small change per gallon becomes a large fleet expense

- Most carriers have limited room to absorb the increase

- The first impact appears in freight contracts, not store prices

- Food supply chains have repeated diesel exposure

- Cross-border trade adds another channel

- Employment and margins are the immediate risks

- The $5 threshold is less important than duration

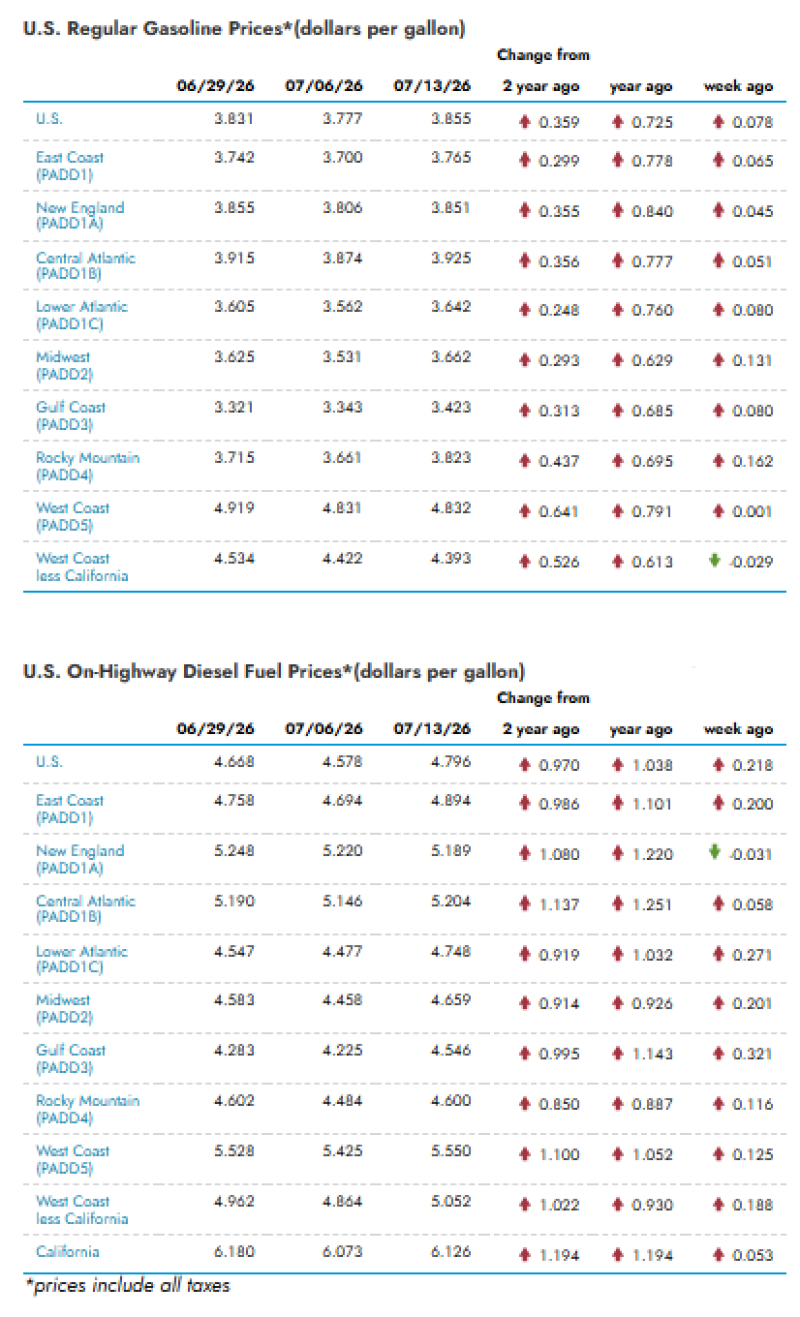

GasBuddy’s national measure has already moved back to roughly $5 per gallon. The more important issue is not the headline threshold itself, but the speed and breadth of the increase.

Diesel prices rose in every major U.S. region during the latest week. That raises costs for trucking companies, distributors and retailers at the same time, leaving fewer parts of the supply chain insulated from the increase.

The national average understates the regional strain

Diesel prices vary sharply across the country. California recorded an average of $6.126 per gallon, up $1.194 from a year ago. The West Coast average stood at $5.550, while the Central Atlantic reached $5.204 and New England averaged $5.189.

Even the least expensive major region was well above previous-year levels. Gulf Coast diesel averaged $4.546, an increase of $1.143 per gallon from a year earlier. The Midwest reached $4.659, while the Lower Atlantic rose to $4.748.

The weekly increase was also substantial in several freight-heavy regions. Gulf Coast prices rose 32.1 cents, the Lower Atlantic gained 27.1 cents, and the national average increased 21.8 cents. For trucking companies operating across several states, the increase is therefore not limited to a few expensive coastal markets. Fuel costs are rising along national distribution routes.

A small change per gallon becomes a large fleet expense

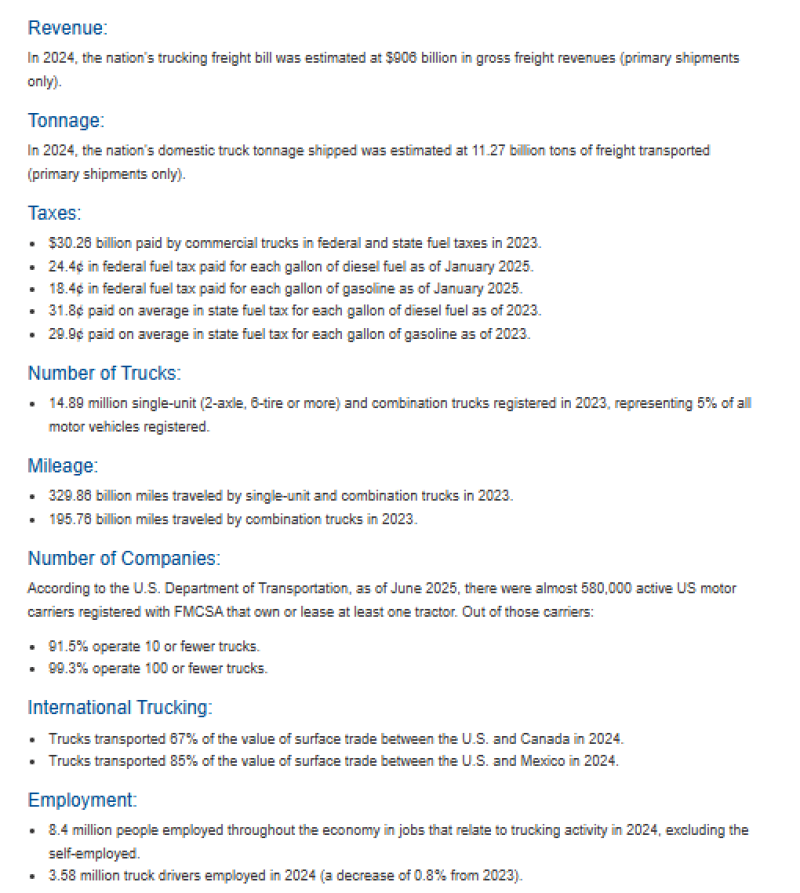

Trucking is a $906 billion industry that moved an estimated 11.27 billion tons of domestic freight in 2024, according to the American Trucking Associations.

The scale of the industry magnifies changes in fuel prices. The United States had approximately 14.89 million registered single-unit and combination trucks in 2023. Those vehicles traveled almost 329.9 billion miles, including 195.76 billion miles traveled by combination trucks.

A tractor consuming thousands of gallons a year creates a very different cost exposure from a passenger car. Across a fleet, an increase of more than $1 per gallon can add millions of dollars to annual operating expenses.

Carriers generally try to recover part of that increase through fuel surcharges. The recovery is not always immediate or complete, particularly for smaller operators working under fixed-price contracts or in weak freight markets.

Most carriers have limited room to absorb the increase

The trucking market is highly fragmented. As of June 2025, nearly 580,000 active U.S. motor carriers owned or leased at least one tractor. Of those companies, 91.5% operated 10 or fewer trucks, while 99.3% operated no more than 100.

That matters because smaller fleets usually have less purchasing power, weaker access to fuel hedging and fewer routes over which to spread higher operating costs. A rapid fuel increase can therefore affect cash flow before freight contracts are repriced.

Large carriers may negotiate fuel programs or pass costs to customers through established surcharge formulas. Owner-operators and small regional fleets are more exposed to the timing difference between paying higher pump prices and recovering those costs from shippers.

The first impact appears in freight contracts, not store prices

Higher diesel prices do not move directly and immediately into the Consumer Price Index. They first affect the cost of transporting raw materials and finished goods.

Manufacturers pay more to receive components. Food distributors pay more to operate refrigerated routes. Retailers face higher replenishment and warehouse-transfer costs. Importers also pay more to move goods from ports and rail terminals to distribution centers.

Businesses then decide whether to absorb the increase, reduce another expense or raise prices.

The outcome depends on margins and pricing power. A retailer selling high-margin discretionary products may absorb part of the increase. A distributor of low-margin groceries or building materials has less flexibility because freight represents a larger share of the final price.

The longer diesel remains elevated, the more likely higher fuel costs are to appear in contract renewals and product prices.

Food supply chains have repeated diesel exposure

Food can accumulate diesel costs at several stages. Fuel is used in agricultural machinery, transport from farms, deliveries to processing facilities, refrigerated distribution and final shipment to supermarkets and restaurants. Products that are heavy, perishable or moved over long distances are particularly exposed.

The effect is not limited to the truck making the final delivery. The same product may be transported several times before reaching a consumer.

Higher diesel prices can therefore pressure grocery margins even when commodity prices remain stable. Retailers may initially resist price increases to protect sales volumes, but sustained transportation costs make that position harder to maintain.

Cross-border trade adds another channel

Trucks transported 67% of the value of U.S. surface trade with Canada in 2024 and 85% of surface trade with Mexico, according to the ATA data.

That gives diesel prices a role in the cost of North American manufacturing as well as domestic retail distribution. Automotive parts, agricultural products, machinery and consumer goods regularly cross borders by truck, sometimes more than once during production.

Higher fuel costs can raise the expense of both importing components and distributing completed products. Companies with complex regional supply chains may face diesel exposure at multiple points before a product reaches the end customer.

Employment and margins are the immediate risks

The trucking industry supports approximately 8.4 million jobs, including 3.58 million truck drivers. Higher fuel prices do not automatically cause job losses, but they intensify pressure on companies already managing equipment, insurance, labor and financing costs.

For carriers unable to recover fuel expenses, the first effects are likely to be lower margins, reduced investment and tighter operating budgets. Some may cut less profitable routes or delay truck purchases and maintenance spending.

Retailers and manufacturers will also face different outcomes. Companies with strong pricing power can pass through higher freight costs. Businesses competing primarily on price may have to accept weaker margins.

The $5 threshold is less important than duration

A brief diesel spike can be managed through surcharges, inventories and short-term cost controls. A sustained period near $5 is more difficult.

The current EIA data already show a broad regional increase, with the national average more than $1 above its year-earlier level. The trucking data show why that increase matters: the industry moves more than 11 billion tons of freight, operates almost 15 million trucks and is dominated by small carriers with limited capacity to absorb abrupt cost changes.

The next stage will be visible in freight rates, corporate margin commentary and retail pricing. Diesel does not need to rise much further to create additional pressure. It only needs to remain expensive long enough for higher transportation costs to be written into new contracts.

Artem Voloskovets

Artem Voloskovets