Artem Voloskovets

Artem Voloskovets

The headline says the UK remains Europe's largest venture capital market. The numbers tell a more interesting story.

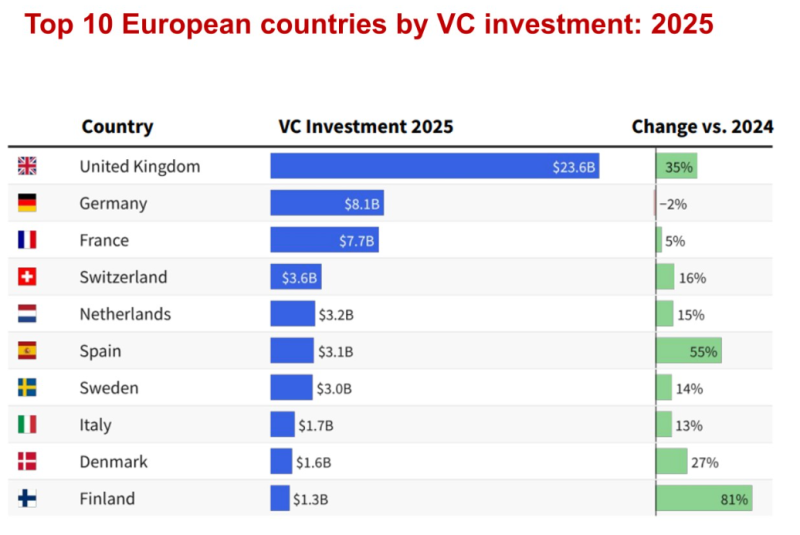

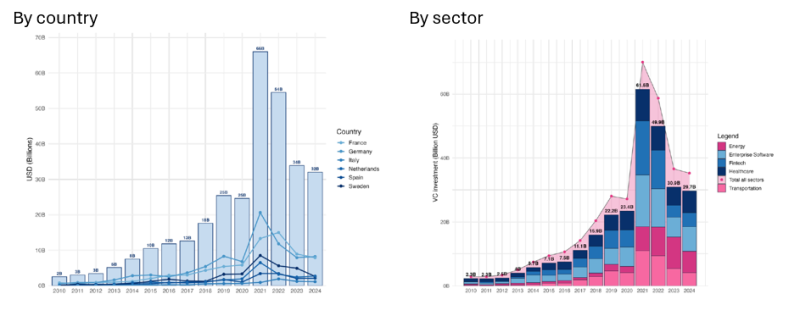

British startups attracted $23.6 billion in VC funding in 2025, nearly three times Germany's $8.1 billion and France's $7.7 billion. More importantly, the gap is widening. UK funding increased 35% year-over-year, while Germany slipped 2% and France grew only 5%.

The usual explanation is that London remains Europe's financial capital. The data suggests something else: venture capital is becoming increasingly concentrated in a small number of ecosystems, while much of Europe is being left behind.

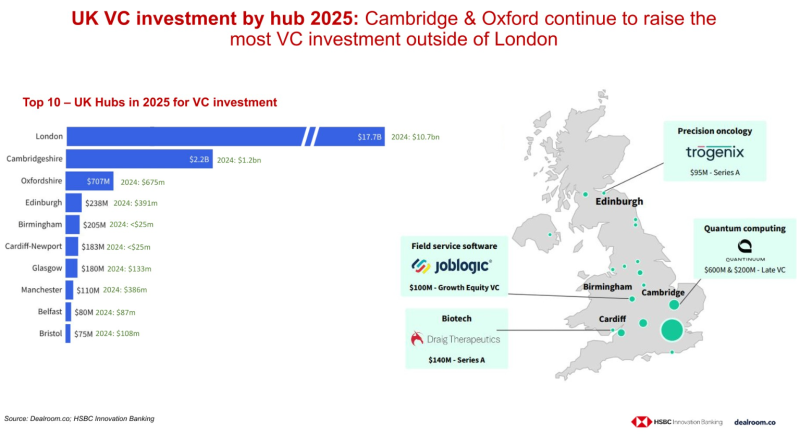

The first sign appears inside the UK itself. London alone attracted $17.7 billion in venture funding this year. That's roughly 75% of all UK VC investment. Yet the most revealing number is not London's. Cambridgeshire raised $2.2 billion, up from $1.2 billion a year ago. Oxfordshire added another $707 million. Combined, those two research-driven hubs attracted almost $3 billion. That is more venture capital than Sweden ($3.0 billion) and nearly equal to the Netherlands ($3.2 billion).

This is where the traditional country ranking starts to break down. Investors are not allocating capital to nations. They are allocating capital to clusters.

Cambridge is competing less with Manchester or Birmingham than with Berlin, Paris, Stockholm, and Zurich. The same dynamic is emerging around Oxford, where AI, biotech, and quantum computing startups are attracting funding far beyond what local population size would suggest.

The map accompanying the UK data highlights the sectors receiving attention: quantum computing, biotech, precision oncology, and enterprise software. Those sectors have one thing in common. They require years of research before they generate meaningful revenue. During the 2021 venture boom, capital chased software companies that could scale quickly. In 2025, money is increasingly flowing toward technologies that are difficult to replicate. The winners are no longer companies with the fastest customer acquisition. They are companies with the strongest intellectual property. That shift is visible across Europe.

The countries posting the strongest growth are not necessarily the largest economies. Finland's venture market expanded 81% year-over-year. Spain grew 55%. Denmark increased by 27%. At first glance, those numbers suggest broad-based recovery. The absolute figures suggest otherwise. Finland's entire VC market reached $1.3 billion. Denmark attracted $1.6 billion. Spain raised $3.1 billion. The growth rates look impressive because they start from relatively small bases. Meanwhile, the UK added roughly $6 billion in additional capital in a single year.

This is creating a three-tier European venture market. The first tier consists of London and a handful of dominant hubs capable of attracting global capital. The second tier includes specialized research clusters such as Cambridge, Oxford, Zurich, and parts of the Nordic region.

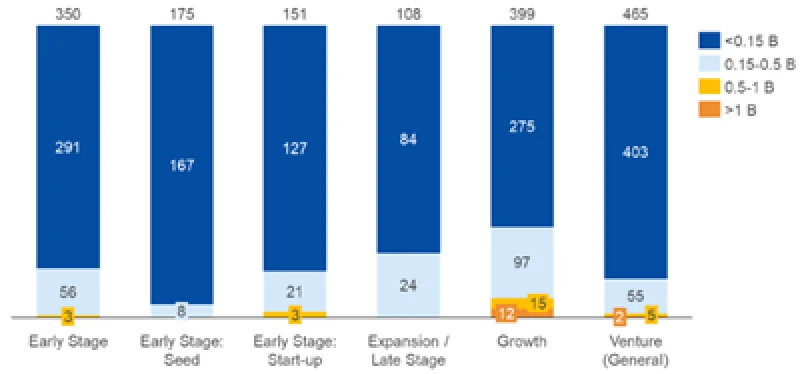

The third tier contains the majority of Europe, where startup activity exists but struggles to attract late-stage investment. The stage data reinforces this trend. Early-stage activity remains relatively broad across the ecosystem. Hundreds of seed and startup-stage deals continue to be completed. But the largest funding rounds are becoming increasingly selective.

The number of billion-dollar-plus transactions remains extremely small relative to the overall market. Yet those deals account for a disproportionate share of total capital deployed.

That is not the profile of a venture boom. It is the profile of a market concentrating around perceived winners. Investors are writing larger checks, but for a narrower group of companies. This matters because AI, quantum computing, biotech, and advanced infrastructure businesses require far more capital than the software startups that dominated the previous decade.

The result is a venture market that increasingly rewards ecosystems capable of supporting companies through multiple funding rounds, not just helping them get started. That may explain why London's lead continues to expand. The UK is no longer winning simply because it produces startups. Germany, France, and the Nordics produce plenty of startups. The UK is winning because investors believe it remains the most reliable place in Europe to finance companies after they leave the garage.

The 2025 numbers suggest European venture capital is entering a new phase. The question is no longer which country can create the most startups. The question is which ecosystem can keep funding them when they become expensive.

Artem Voloskovets

Artem Voloskovets