Marina Lubimova

Marina Lubimova

The government's decision to lift its 2025 GDP growth forecast to 2.6% is more than an upgraded projection. It reflects an economy that has consistently outperformed every major eurozone peer despite weaker global trade, tighter financial conditions and persistent geopolitical uncertainty. The question is no longer why Spain is growing faster.

The question is why the gap continues to widen.

Growth That Refuses to Slow

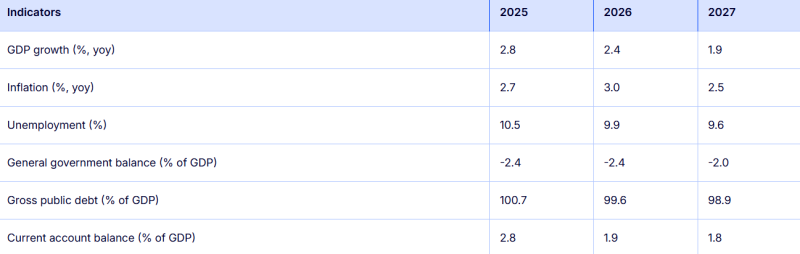

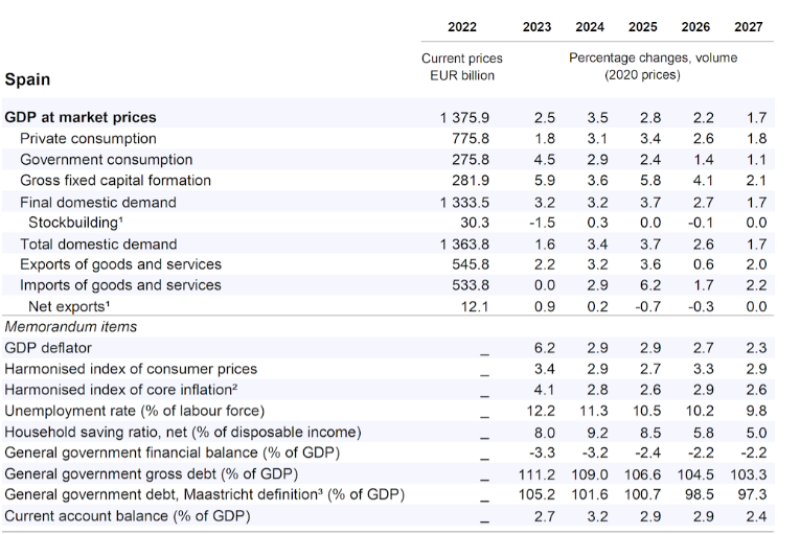

Spain's economy continues to move against the European cycle. While Germany remains constrained by weak industrial production and the broader eurozone is expected to expand by less than 1%, Spain is projected to grow 2.6% in 2025, before moderating to 2.2% in 2026. Even the Bank of Spain's more cautious forecast still implies growth of 2.3% next year.

That consistency matters more than the absolute number. Three consecutive years of expansion above the eurozone average suggest Spain is benefiting from structural advantages rather than a temporary rebound.

More Than a Tourism Story

Tourism still receives most of the attention. It no longer explains most of the economy. Growth is increasingly supported by household consumption, immigration, business investment, and public spending financed through the EU Recovery Fund. Together, these drivers have created a broader economic base than Spain relied on during previous expansion cycles.

The result is an economy less dependent on any single sector and better positioned to absorb external shocks.

Strong Numbers Beneath the Headline

Headline GDP growth tells only part of the story. OECD projections show unemployment continuing to decline while public debt gradually falls over the next several years. Those trends rarely occur simultaneously in economies expanding well above the regional average. Lower debt also gives policymakers greater flexibility should external conditions deteriorate.

Expansion Is Becoming More Balanced

Rapid recoveries rarely last forever. Spain's recovery does not need to. The Bank of Spain expects domestic demand to cool after several years of exceptional strength. Household consumption is slowing, investment growth is normalizing, and imports are no longer rising as quickly.

That does not necessarily imply weaker fundamentals. Instead, the composition of growth is shifting. External demand is beginning to offset softer domestic activity, reducing the economy's dependence on consumer spending alone. A slower pace of expansion could ultimately prove more sustainable than another year of above-trend growth.

The Next Constraint

Growth is no longer Spain's primary challenge. Inflation is. Higher energy prices have already prompted the Bank of Spain to revise its inflation outlook upward, increasing the risk that interest rates remain elevated for longer than markets previously expected.

A prolonged slowdown across Europe would create another headwind. Although Spain has been one of the continent's strongest performers, it remains deeply integrated into the eurozone economy.

Read more: The Digital Tax Battle Is Reshaping Global Trade — Trump's 100% Tariff Threat Is Just the Beginning

Europe's New Benchmark?

Spain's economic profile has changed in ways that were difficult to imagine a decade ago. The economy is no longer defined by post-crisis recovery. It is increasingly supported by a diversified mix of consumption, investment, services and labor-market expansion.

Growth is expected to moderate over the coming years. That is typical for a mature expansion.

The more significant development is that Spain now enters this slower phase with stronger public finances, falling unemployment and one of the highest growth rates among advanced European economies. That combination is becoming increasingly uncommon across the eurozone.

Marina Lubimova

Marina Lubimova