Artem Voloskovets

Artem Voloskovets

The Federal Reserve has pursued an unusually difficult objective: slowing the labor market enough to ease inflation without pushing the economy into recession. June's employment report suggests that balance is beginning to emerge.

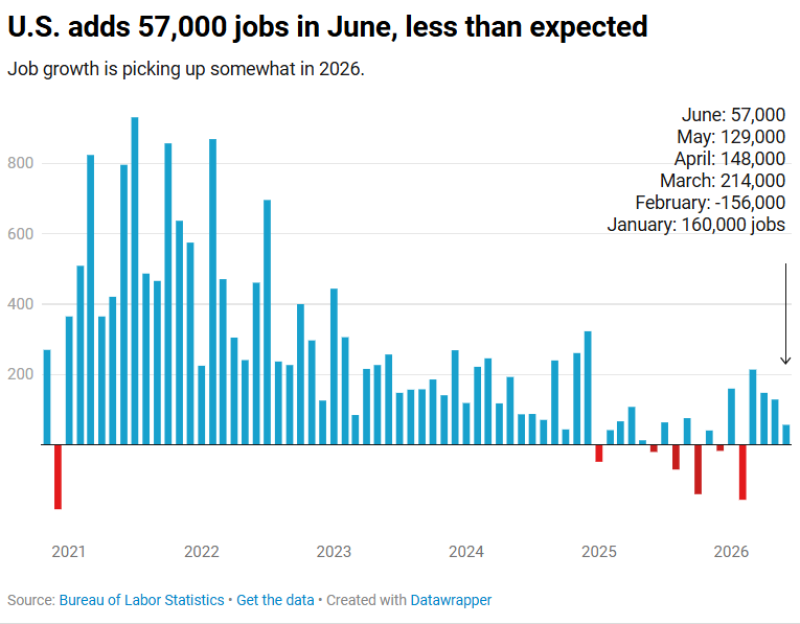

Nonfarm payrolls increased by 57,000, unemployment held at 4.2%, wage growth remained positive, and layoffs stayed historically subdued. Hiring has slowed sharply from the post-pandemic surge, yet the adjustment is taking place through fewer new positions rather than widespread job losses. This is neither an overheating labor market nor one in recession. It is a labor market settling into a lower gear.

A Smaller Engine

The headline number naturally draws attention, but the broader trend is more revealing. Monthly payroll gains that routinely exceeded 500,000 during 2021 and early 2022 have given way to modest, increasingly stable growth. June's 57,000 jobs, following revised gains of 129,000 in May and 148,000 in April, fit comfortably within that pattern.

The post-pandemic hiring frenzy has ended. What replaced it is a labor market capable of generating employment without the urgency that defined the recovery years. For policymakers, slower hiring has always been preferable to rising unemployment. June suggests that distinction is becoming reality.

Where Demand Still Exists

The composition of hiring explains why the headline figure looks weaker than the underlying economy. Professional and Business Services created 36,000 jobs, extending a recovery that has added 172,000 positions since October 2025. Social Assistance contributed 25,000, while Health Care added 22,000, although hiring in the sector has slowed from last year's pace. The weakness came almost entirely from Leisure and Hospitality, which lost 61,000 jobs after weaker-than-normal seasonal recruitment. The distinction is important. Businesses are not broadly reducing payrolls they are becoming more selective about adding new workers.

The Trend Changed Before June

The strongest signal in the report appears near the bottom. April payroll growth was revised lower by 31,000 jobs. May lost another 43,000. Combined, the revisions removed 74,000 jobs from previously published estimates. Rather than producing a single disappointing report, the labor market has been cooling for several months. June simply made that trend difficult to ignore.

Hiring Is Slowing Faster Than Employment

Payroll growth tells only part of the story. The broader labor market continues to operate with relatively low layoffs, stable unemployment claims, and fewer available vacancies than during the post-pandemic expansion.

Businesses appear increasingly willing to retain experienced employees while delaying expansion plans and slowing recruitment. That combination produces an unusual labor market. Workers already employed face relatively little risk of losing their jobs. Workers searching for new opportunities face a noticeably more competitive environment. The adjustment is occurring through hiring decisions rather than layoffs.

Exactly the Adjustment the Fed Wanted

Throughout the tightening cycle, policymakers argued that labor demand, not employment itself, needed to cool. June's report closely matches that outcome. Payroll growth has slowed.

Vacancies continue to normalize. Wage growth remains positive at 3.5% year-over-year rather than accelerating. Unemployment has stabilized instead of rising sharply. Inflation can ease under those conditions without requiring a severe deterioration in employment.

For much of the past three years, economists questioned whether such an outcome was achievable. The latest report suggests it may be.

Not Victory - Progress

None of this guarantees a soft landing. Inflation remains above the Federal Reserve's target, while business investment and consumer spending continue to face pressure from restrictive monetary policy. The labor market could still weaken further if growth slows more sharply during the second half of the year. For now, however, the adjustment remains orderly. Higher interest rates are reducing demand for labor without triggering the wave of layoffs that has accompanied many previous tightening cycles.

Conclusion

June's payroll report is easy to dismiss as another downside surprise. Viewed in isolation, 57,000 jobs certainly look underwhelming. Viewed alongside unemployment, wages, industry data, revisions, and broader labor market indicators, the report tells a different story. The Federal Reserve never set out to stop hiring altogether. It set out to remove excess demand from one of the hottest labor markets in decades. June offers some of the strongest evidence yet that this process is unfolding largely as intended. The hiring boom is over, but the labor market has yet to break a balance that once seemed unlikely, and one that now looks increasingly achievable.

Artem Voloskovets

Artem Voloskovets