Artem Voloskovets

Artem Voloskovets

Yet the auction delivered a useful signal about something larger than government funding costs. Despite a steady stream of warnings about rising deficits, expanding debt issuance, and tighter financial conditions, investors continue to absorb large amounts of short-term Treasury debt without demanding higher compensation. That is becoming increasingly difficult to ignore.

The Treasury Didn't Need To Pay Up

The Treasury sold the same amount of debt as it did a week earlier, $70 billion, but paid a slightly lower rate to do it. The auction cleared at 3.58%, down from 3.595% in the previous sale. Meanwhile, the bid-to-cover ratio slipped from 3.13 to 2.99.

Auction Results

| Metric | Current Auction | Previous Auction |

| Amount Offered | $70.0B | $70.0B |

| Bid-to-Cover | 2.99 | 3.13 |

| High Rate | 3.58% | 3.595% |

| Settlement Date | June 30 | June 24 |

Bid-to-cover ratio declined from 3.13 to 2.99 while the auction rate eased from 3.595% to 3.58%. The decline in demand was modest. More importantly, it wasn't large enough to push funding costs higher. If investors were becoming uncomfortable with the pace of Treasury issuance, higher yields would likely be required to attract buyers. That did not happen. Instead, the Treasury borrowed the same amount of money at a slightly lower rate.

Three And A Half Percent Is Still Competitive

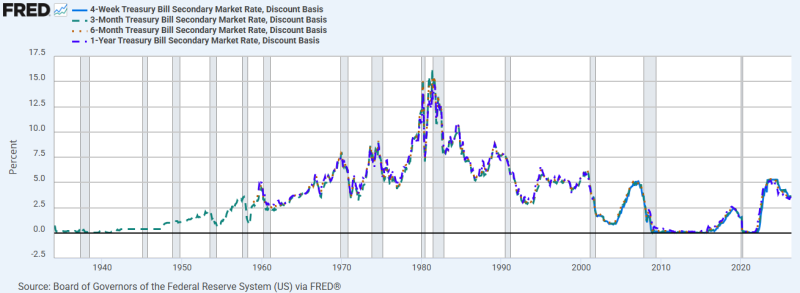

The current 4-week bill yield may not look extraordinary compared with the peaks reached during the Federal Reserve's tightening cycle, but historical context tells a different story.

For most of the period between 2009 and 2021, investors earned little or nothing on short-dated government debt. Today's auction cleared at a yield that would have been considered unusually attractive throughout most of that era.

The chart highlights three realities:

- Short-term Treasury yields spent much of the post-financial-crisis period near zero.

- The Fed's inflation-fighting campaign pushed bill yields above 5%.

- Even after declining from those highs, the current 3.58% yield remains elevated by historical standards.

For money-market funds, corporate treasurers, banks, and institutional cash managers, Treasury bills still offer a compelling combination of liquidity, safety, and income. That helps explain why demand remains resilient even as yields drift lower.

The Foreign Buyer Hasn't Left

Predictions of a global retreat from U.S. government debt have become a recurring feature of financial commentary. The data continue to point in the opposite direction.

Foreign holdings of U.S. Treasuries rose to $9.352 trillion in April, up from $9.348 trillion in March and roughly 4% above year-earlier levels.

| Month | Holdings |

| March 2026 | $9.348T |

| April 2026 | $9.352T |

The increase was not dramatic, but it reinforces a broader trend. International investors remain willing buyers of U.S. government debt despite persistent concerns about fiscal deficits and expanding Treasury issuance. That matters because growing borrowing needs become much easier to manage when demand continues to expand alongside supply.

The Market Isn't Asking For A Premium

Treasury auctions tend to reveal stress long before policymakers acknowledge it. When liquidity becomes scarce or investor confidence deteriorates, the symptoms are usually visible:

- yields move higher;

- participation weakens sharply;

- borrowing costs rise.

The latest auction showed none of those characteristics. Demand softened, but only marginally. Funding costs moved lower rather than higher. Investors continued to allocate capital toward short-term government securities even as supply remained substantial.

For now, the market is not demanding a premium to absorb additional Treasury debt. That may be the most important takeaway from the entire auction.

Not The Signal The Fed Needs To Worry About

Financial markets often focus on Federal Reserve statements, projections, and speeches. Treasury auctions provide a different kind of information. They show how investors behave when real money is put to work.

Nothing in the latest bill sale suggests a funding-market problem that would require attention from policymakers. If anything, the results point to a system that remains capable of absorbing new Treasury issuance without significant friction. That does not eliminate long-term fiscal concerns. It simply suggests those concerns are not yet translating into funding stress.

Artem Voloskovets

Artem Voloskovets