Sergey Diakov

Sergey Diakov

The latest U.S. labor market report delivered a mixed but highly important signal for Wall Street: hiring remains stronger than expected, but wage inflation continues to cool.

April nonfarm payrolls came in at 115,000 versus expectations of 65,000, while the unemployment rate held steady at 4.3%, matching forecasts. Meanwhile, average hourly earnings rose just 0.2% month-over-month and 3.6% year-over-year, both below consensus estimates.

The numbers reinforce the idea that the U.S. economy is slowing gradually rather than collapsing - a scenario markets increasingly view as the ideal “soft landing.”

One of the biggest takeaways from the report is the continued decline in wage pressure. The latest hourly earnings data shows wage growth steadily trending lower from post-pandemic highs near 6%, approaching levels closer to the Fed’s long-term inflation comfort zone.

That matters because wage inflation has been one of the Federal Reserve’s biggest concerns over the past several years. Slower earnings growth could give policymakers more confidence that inflation is cooling without a major spike in unemployment.

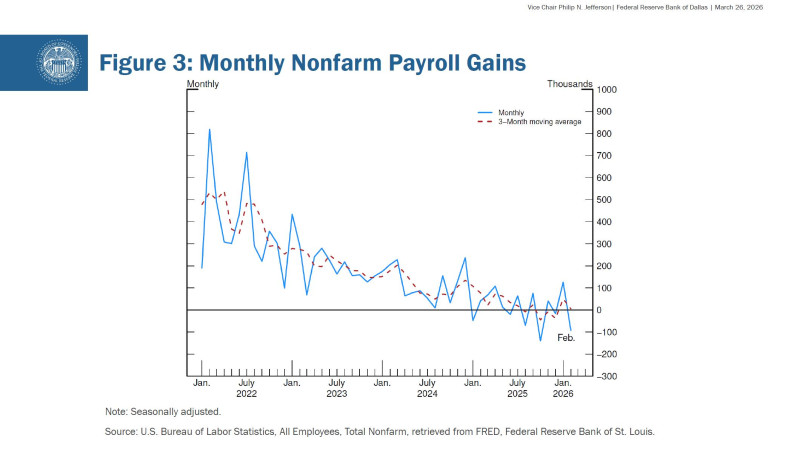

At the same time, payroll growth remains resilient. The latest Fed labor market charts show monthly nonfarm payroll gains slowing significantly compared to the explosive hiring seen in 2022, but the labor market is still producing jobs at a pace strong enough to avoid immediate recession fears.

For investors, that creates a delicate balancing act.

- Lower wage growth is supportive for risk assets including stocks and crypto because it may reduce Treasury yields and revive expectations for Fed rate cuts.

- Stable unemployment signals that consumer demand and broader economic activity remain intact, limiting fears of an immediate downturn.

- Stronger-than-expected payroll growth may prevent the Federal Reserve from cutting rates too aggressively in the near term.

The next major catalyst for markets will now be upcoming CPI inflation data and Federal Reserve commentary. If inflation continues cooling while employment remains stable, the latest jobs report could strengthen the soft-landing narrative that has fueled risk assets throughout 2025.

Sergey Diakov

Sergey Diakov