Marina Lubimova

Marina Lubimova

That shift matters because equity valuations, Treasury yields and borrowing costs all depend on how long the Fed keeps monetary policy restrictive.

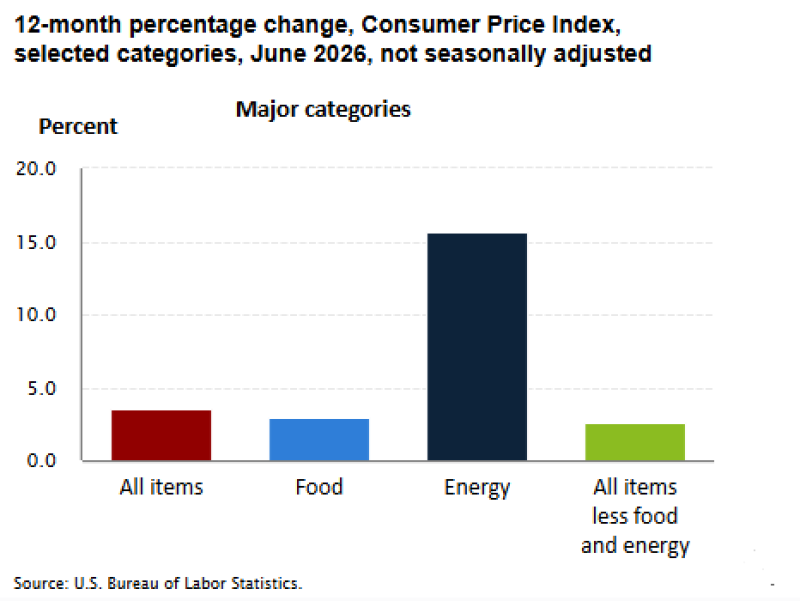

Inflation Is Cooling, but Not Evenly

June inflation data show clear progress toward price stability, although several components continue moving in different directions. Headline CPI increased 3.4% year over year, while core CPI, which excludes food and energy, slowed to 2.7%, bringing it closer to the Fed's target. Food prices rose 3.0%, but energy prices jumped 15.5%, the strongest increase among the major categories.

The contrast explains why Fed officials remain cautious. Core inflation is gradually easing, yet the sharp rebound in energy prices creates the risk of renewed inflationary pressure across transportation, manufacturing and consumer goods. A single month of favorable data is unlikely to convince policymakers that inflation has been fully contained.

Why the 2% Goal Still Matters

The debate is no longer about whether inflation is falling — it is about how much inflation the Federal Reserve is willing to accept over the long run. Some economists have suggested raising the inflation target to 3%, arguing that it would give the central bank greater flexibility to lower interest rates while supporting economic growth.

Warsh's remarks point in the opposite direction. Maintaining a strict 2% target reinforces confidence that inflation will eventually return to pre-pandemic levels instead of settling permanently above them.

That credibility shapes borrowing costs, wage negotiations and long-term investment decisions throughout the economy. If markets begin to doubt the Fed's commitment, inflation expectations could rise even before actual prices accelerate.

Interest Rates Could Stay Restrictive

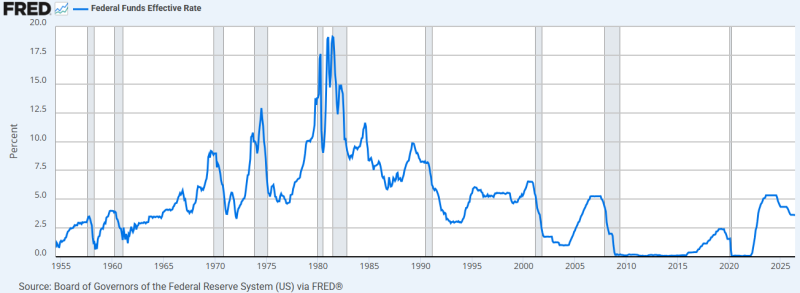

Warsh's comments also challenge the assumption that lower inflation automatically leads to lower interest rates. The Federal Funds Effective Rate remains close to 3.3%, well above the levels that prevailed for most of the decade before the pandemic. Although policy has become less restrictive than at the peak of the tightening cycle, monetary conditions remain historically tight.

The historical record supports a cautious approach. During previous inflation cycles, particularly in the late 1970s and early 1980s, the Federal Reserve kept rates elevated for years before inflation expectations were fully restored. Warsh's commitment suggests that preventing another inflation rebound is likely to take priority over delivering rapid policy easing.

High-Valuation Stocks Face Greater Pressure

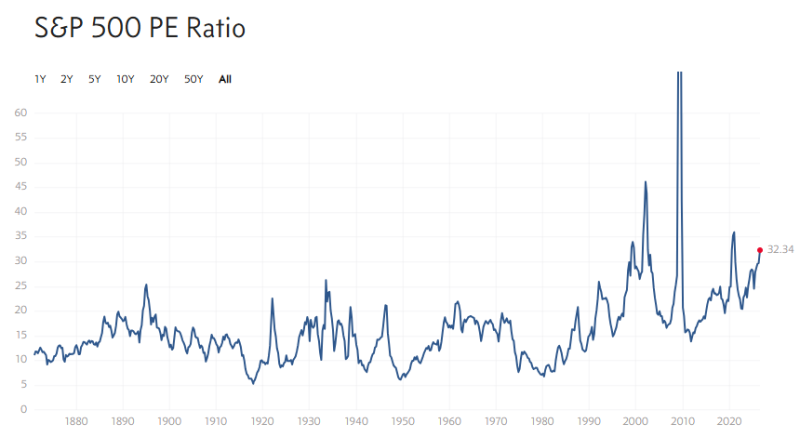

Equity markets have benefited from expectations that borrowing costs will gradually decline over the next several quarters. Current valuations leave little margin for disappointment.

The S&P 500 trades at a price-to-earnings ratio of roughly 32.3, significantly above its long-term historical average. Investors are therefore paying a premium based on expectations of resilient earnings, stable economic growth and eventually lower interest rates.

If policy remains restrictive longer than markets anticipate, those assumptions become harder to justify. Higher interest rates increase the discount rate applied to future earnings, making richly valued technology and growth companies particularly sensitive to changes in Fed policy.

Investors May Need to Reprice Risk

Warsh did not indicate that another rate hike is imminent. His message is that policy should remain focused on eliminating inflation rather than responding to short-term market expectations.

Future decisions will depend on incoming data, including inflation, wages and labor-market conditions. Any renewed strength in price pressures could postpone future rate cuts, while sustained improvement would strengthen the case for gradual easing.

That leaves investors in a market where every inflation report carries greater significance than before.

Credibility Is Becoming the Main Policy Tool

The significance of Warsh's comments extends beyond the numerical target itself.

A central bank's ability to control inflation depends on whether households, businesses and investors believe it will follow through on its commitments. Once that confidence weakens, inflation expectations can become embedded in wages, contracts and corporate pricing decisions.

By publicly reaffirming the 2% objective, Warsh is emphasizing that restoring price stability remains the Federal Reserve's primary objective.

Marina Lubimova

Marina Lubimova