Marina Lubimova

Marina Lubimova

The company reported preliminary second-quarter revenue of $20.23 billion, compared with $18.61 billion a year earlier. Net income reached $1.699 billion, while diluted earnings per share increased to $7.62, extending the earnings growth seen earlier this year.

Rather than the quarterly numbers, investors are likely to focus on the company's revised full-year guidance, which cuts earnings expectations while leaving revenue forecasts largely unchanged.

Strong Operating Trends Continue

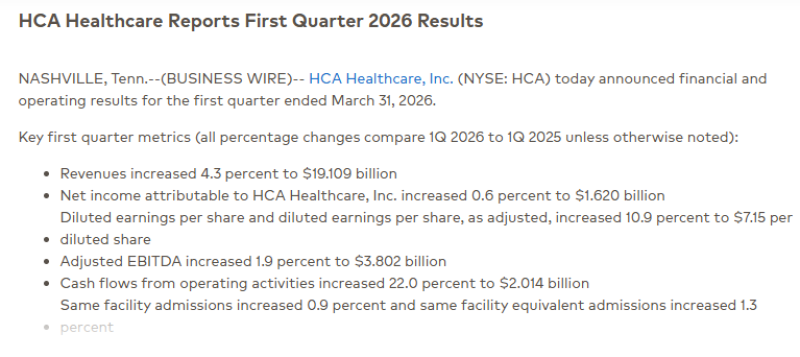

The second quarter followed a solid start to 2026. During the first quarter, revenue rose 4.3% year over year to $19.11 billion. Diluted EPS climbed 10.9% to $7.15, adjusted EBITDA reached $3.80 billion, and operating cash flow increased 22% to $2.01 billion. Patient activity also remained healthy, with same-facility admissions growing 0.9% and equivalent admissions increasing 1.3%.

The preliminary second-quarter figures suggest those trends remained intact. Revenue moved above $20 billion, while earnings per share improved again, indicating that patient volumes and operational execution continued to support financial performance.

Revenue Holds Up While Earnings Expectations Decline

The updated annual guidance reveals a clear divergence between expected revenue and expected profitability.

| Metric | Previous Guidance | Revised Guidance |

| Revenue | $76.5B–80.0B | $77.0B–79.5B |

| Net Income | $6.495B–7.035B | $6.30B–6.70B |

| Adjusted EBITDA | $15.55B–16.45B | $15.40B–16.10B |

| Diluted EPS | $29.10–31.50 | $28.70–30.50 |

Revenue guidance was narrowed rather than reduced. The midpoint of the forecast remains close to previous expectations and near Wall Street consensus.

Profit forecasts tell a different story. Management lowered projected net income, adjusted EBITDA and diluted EPS, pointing to weaker margins rather than weaker business activity.

Costs Are Becoming the Bigger Variable

Keeping revenue guidance largely intact while trimming profit expectations suggests that HCA expects expenses to rise faster than revenue during the second half of the year.

The company also disclosed that changes in exchange coverage and a lower volume of uninsured patients are expected to reduce second-quarter pre-tax income by roughly $400 million. Although that shift reflects changes in payer mix rather than hospital demand, it highlights how reimbursement dynamics can materially affect earnings.

Labor costs, reimbursement rates and inflation remain the primary variables for hospital operators. HCA continues to benefit from its scale and operational efficiency, but the updated guidance suggests those advantages may not fully offset cost pressures over the remainder of 2026.

The Focus Shifts to Margins

The second-quarter results confirm that HCA's business continues to expand. Revenue is growing, admissions remain positive, and earnings continue to exceed $7 per share on a quarterly basis.

The more important question now is how much of that revenue growth will translate into profit during the second half of the year.

Management's updated outlook suggests margins are likely to tighten despite stable demand. Investors will therefore pay close attention to the full earnings report for additional detail on labor expenses, reimbursement trends, operating margins and the assumptions behind the revised guidance.

Marina Lubimova

Marina Lubimova