Marina Lubimova

Marina Lubimova

Combined with the rest of the economic data, it tells a different story. Consumer spending is still expanding, GDP growth has been revised higher, and the Federal Reserve has significantly raised its own inflation forecasts. Together, these signals point to an economy that remains too resilient for inflation to cool on its own. The policy challenge is no longer understanding why prices are high. It is determining how long demand can stay this strong under restrictive monetary policy.

Demand Hasn't Slowed Enough

Inflation persists when demand continues to outpace the economy's ability to absorb it. That appears to be today's environment. Consumer spending rose 0.3% in May, extending a pattern of resilient household demand despite elevated interest rates. Strong employment and steady income growth continue to support consumption, limiting the slowdown policymakers expected from tighter financial conditions. The implication is straightforward. Inflation is proving difficult to reduce because the economy has yet to experience a meaningful loss of momentum.

Growth Is Holding Up Better Than Expected

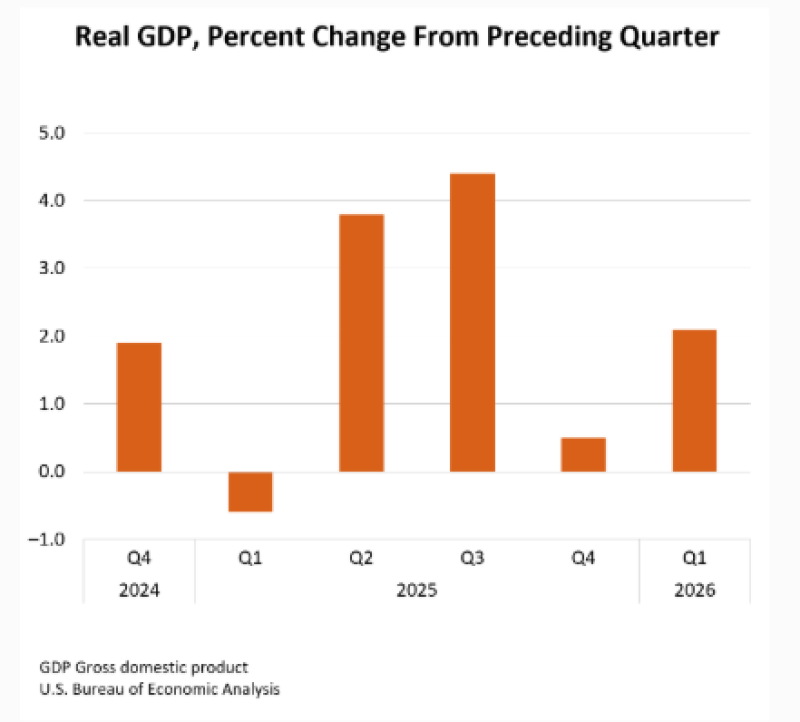

The latest GDP revision reinforces that conclusion. The Bureau of Economic Analysis revised first-quarter growth upward to 2.1%, indicating that activity recovered after slowing late last year.

Economic growth recovered to 2.1% in the first quarter of 2026 after slowing to 0.5% in the previous quarter, highlighting the resilience of domestic demand despite restrictive monetary policy.

Higher interest rates are no longer restraining growth as effectively as expected, reducing confidence that inflation will return to target without an extended period of tight financial conditions.

The Fed Has Revised More Than Its Inflation Forecast

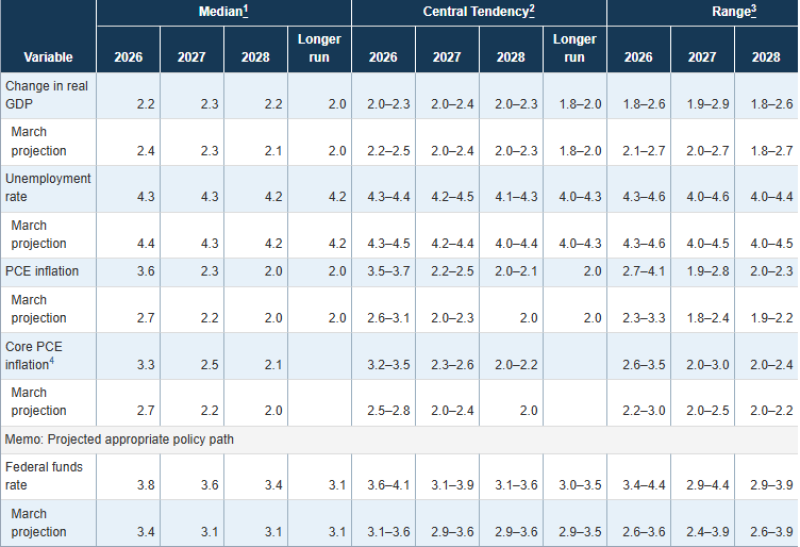

The inflation report attracted immediate attention. The Federal Reserve's updated projections reveal the larger shift. Officials now expect inflation to remain substantially higher than they forecast only one quarter ago, while making only minor adjustments to their growth outlook.

The June projections show a decisive upward revision in inflation expectations while economic growth remains broadly intact, leading policymakers to project a higher policy rate.

Inflation outlook

Median PCE inflation:

- March: 2.7%

- June: 3.6%

Median Core PCE inflation:

- March: 2.7%

- June: 3.3%

These revisions suggest officials no longer expect inflation to move steadily toward the 2% target.

Growth outlook

GDP expectations changed only modestly.

- March: 2.4%

- June: 2.2%

A relatively small downgrade implies that policymakers still see the economy expanding at a healthy pace despite restrictive monetary policy.

Interest-rate outlook

The projected Federal Funds Rate also moved higher.

- March: 3.4%

- June: 3.8%

Taken together, these revisions represent more than a response to one inflation report. They reflect a broader reassessment of how persistent inflation is likely to be.

The Debate May Be Framed Incorrectly

Attention has largely focused on whether another rate hike is coming. That may prove less important than how long rates remain at restrictive levels. An additional increase would marginally tighten financial conditions. A prolonged period of elevated rates would influence corporate refinancing, capital investment, commercial real estate, housing activity and equity valuations over several years. The duration of restrictive policy could matter more than its peak.

The Inflation Story Has Changed

The current cycle differs from the inflation surge of 2022. Earlier price increases were closely tied to supply disruptions and reopening effects. Today's inflation is increasingly supported by resilient domestic demand. Consumer spending remains firm. Economic growth continues. The labor market has yet to weaken meaningfully. That combination makes inflation considerably harder to reverse.

The Real Question Has Shifted

The latest data does not simply indicate that inflation is higher than expected. It suggests the U.S. economy continues to absorb restrictive monetary policy with relatively limited damage. That leaves the Federal Reserve facing a different challenge than markets anticipated earlier this year. The central issue is no longer whether inflation remains above target. It is whether demand can stay this resilient without requiring interest rates to remain elevated well beyond current expectations.

If that answer is yes, markets may have to adjust not to another rate hike, but to an extended period in which monetary policy remains restrictive as the new normal.

Marina Lubimova

Marina Lubimova