Artem Voloskovets

Artem Voloskovets

For most of the AI boom, the investment case was remarkably simple: buy the companies supplying more compute. That logic propelled Nvidia to the center of the market while hyperscalers committed hundreds of billions of dollars to expanding AI infrastructure. The assumption was straightforward: more GPUs meant more AI.

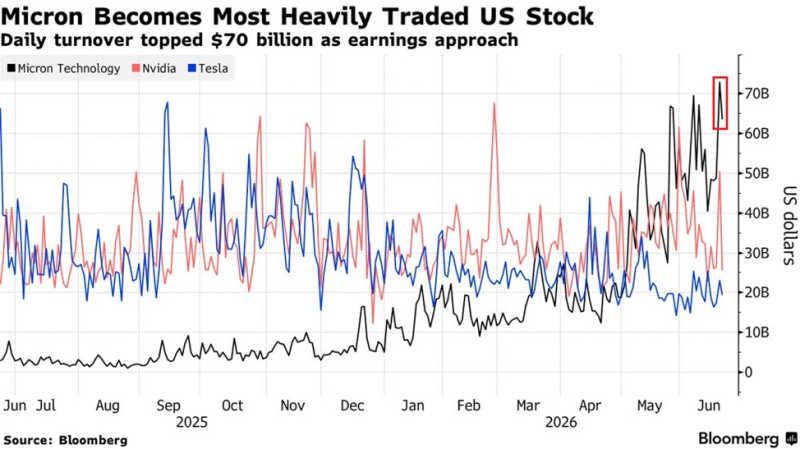

Recent trading activity suggests that the assumption is becoming incomplete. Ahead of its latest earnings report, Micron briefly became the most actively traded stock in the United States, with daily turnover exceeding $70 billion, surpassing both Nvidia and Tesla.

Volume alone doesn't explain why this matters. Markets occasionally trade heavily around earnings. They rarely reallocate this much capital unless investors believe a company now belongs to a different investment theme. That appears to be happening with Micron.

Why Micron Suddenly Trades Like Core AI Infrastructure

For years, Micron was viewed as a classic memory manufacturer, a company whose fortunes rose and fell with DRAM pricing cycles. The Bloomberg chart illustrates how quickly that perception changed.

Throughout most of 2025, Micron's trading activity remained well below Nvidia and Tesla. Beginning early this year, turnover accelerated sharply before peaking above $70 billion in late June.

Such moves usually reflect more than expectations for a single earnings report. They suggest investors are reassessing how an entire industry should be valued. Rather than treating memory as another semiconductor category, the market increasingly sees it as a critical layer of AI infrastructure.

Strategic Contracts Matter More Than Quarterly Results

Micron's financial results were exceptionally strong. Revenue climbed to $41.46 billion, compared with $23.86 billion in the previous quarter and $9.30 billion a year earlier. Operating cash flow more than doubled sequentially, while management projected another quarter of robust growth.

Those figures explain part of the rally. The more consequential announcement was the expansion of Strategic Customer Agreements with major AI customers. Historically, memory manufacturers relied on short-term purchasing cycles, leaving revenues highly sensitive to changing inventories and pricing.

Long-term agreements alter that relationship. Customers reserve production capacity years in advance, while suppliers gain greater visibility into future demand. According to Micron, these agreements now represent approximately $22 billion in customer commitments, providing a level of revenue stability that has been rare in the memory industry. That changes the economics of the business more than any single quarterly report.

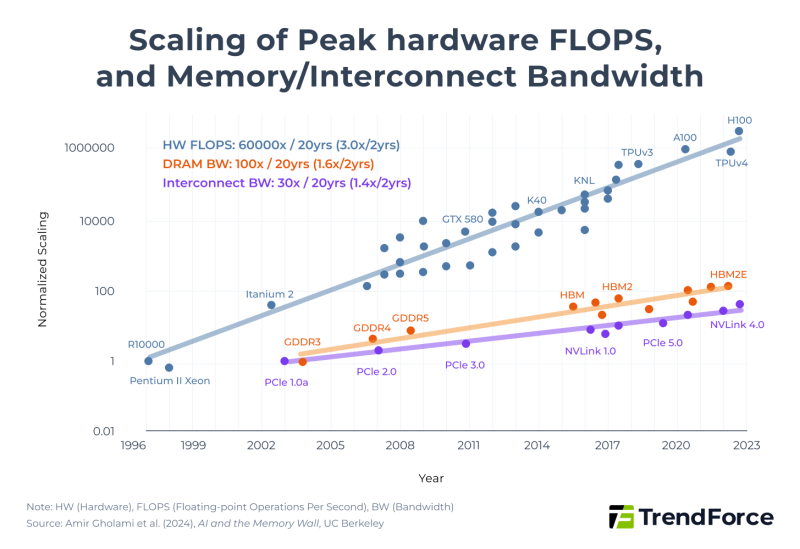

Compute Has Outpaced Memory for Two Decades

The second chart explains why investors are beginning to pay attention.

Over roughly two decades:

- Peak computing performance increased by approximately 60,000×

- DRAM bandwidth improved by roughly 100×

- Interconnect bandwidth increased by about 30×

Those numbers reveal a growing imbalance inside modern computing systems. Processing power has advanced exponentially faster than the infrastructure responsible for supplying processors with data.

As AI models become larger and more complex, that imbalance becomes increasingly expensive. Faster processors deliver diminishing returns if memory systems cannot feed them efficiently. The industry's long-discussed Memory Wall is no longer a theoretical engineering problem. It is becoming an economic one.

The Bottleneck Has Shifted

The first phase of AI infrastructure focused on adding more compute. The next phase is increasingly about improving utilization.

That requires technologies that receive far less public attention than GPUs:

- High-Bandwidth Memory (HBM)

- Advanced DRAM

- Memory packaging

- High-speed interconnects

- Rack-scale memory architectures

Each new generation of AI hardware demands substantially more memory bandwidth than the last. As a result, investment is expanding beyond processors toward the systems that keep those processors operating efficiently. This is less a replacement of the compute story than its natural evolution.

This Isn't Just a Micron Story

Micron happens to be the company drawing attention today. The underlying shift extends much further. Cloud providers continue increasing AI infrastructure spending, while larger language models require more memory capacity and higher bandwidth with every generation.

The value chain is gradually broadening. Companies solving data movement constraints may become increasingly important alongside companies building faster processors. That helps explain why investors are beginning to evaluate memory businesses differently than they did during previous semiconductor cycles.

What the Market May Be Pricing In

Micron's record trading volume is easy to interpret as a reaction to strong earnings. Viewed in isolation, that explanation is reasonable. Placed alongside the industry's changing hardware economics, however, the picture becomes more interesting. The first phase of the AI buildout rewarded companies that expanded computing capacity. The next phase is likely to reward those removing the constraints that prevent that capacity from being fully utilized. Recent trading in Micron suggests the market has started to recognize the difference.

Artem Voloskovets

Artem Voloskovets