Marina Lubimova

Marina Lubimova

The Berkshire Hathaway chairman revealed that buying Alphabet was his own idea while acknowledging the company should have entered Berkshire's portfolio much earlier. What began as a missed opportunity has since become an investment worth roughly $31 billion, making Alphabet Berkshire's third-largest public equity holding, behind Apple and American Express and ahead of Coca-Cola, Bank of America, and Chevron.

I initiated it. I am not doing anything that Greg Abel doesn't approve of. He's not doing anything I don't approve of. We talk all the time, but he is the decider.

The remarks explain not only why Berkshire finally invested in Alphabet but also how investment authority is shifting to Greg Abel.

A Business Berkshire Underestimated

Buffett did not portray Alphabet as a technology success story. Instead, he described it as the type of business Berkshire has always tried to own. He called the delayed investment a mistake because Alphabet already possessed the qualities that have defined Berkshire's biggest winners for decades: consistently high returns on capital and the ability to reinvest earnings into new growth opportunities.

Google Search continues to produce enormous cash flows while requiring relatively little incremental capital. Those profits have funded businesses including Google Cloud, YouTube, Android and the company's rapidly expanding AI infrastructure. Viewed through Buffett's traditional framework, Alphabet looks less like a Silicon Valley growth stock and more like a long-term capital compounding machine.

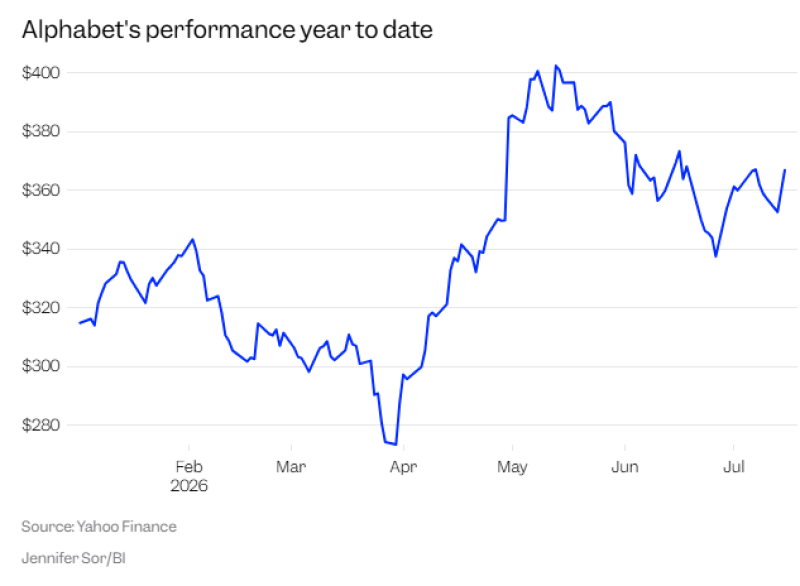

Alphabet shares rebounded from roughly $274 in late March to more than $400 in May before stabilizing around $365–370 in July.

Alphabet's share price reflects that operating strength. After falling sharply during the first quarter, the stock recovered almost 46% over the following weeks, reaching fresh highs above $400 in May. While the rally cooled during June, the shares remained well above their spring lows, trading near $367 in July.

The recovery has been driven by continued strength in Google's advertising business, accelerating cloud growth and investor optimism surrounding Alphabet's AI investments. Those trends reinforce Buffett's point that exceptional businesses continue creating value long after the market questions them.

From Missed Opportunity to Core Holding

Alphabet has evolved into one of Berkshire's most important investments. Its position in the portfolio now exceeds several companies that have been associated with Buffett for decades, including Coca-Cola, Bank of America and Chevron.

The shift says as much about Berkshire's investment philosophy as it does about Alphabet. Buffett has never avoided technology simply because it is technology. His focus has always been on business economics—companies with durable competitive advantages, abundant free cash flow and opportunities to reinvest capital at attractive returns.

Alphabet now fits that description as clearly as any company in Berkshire's portfolio.

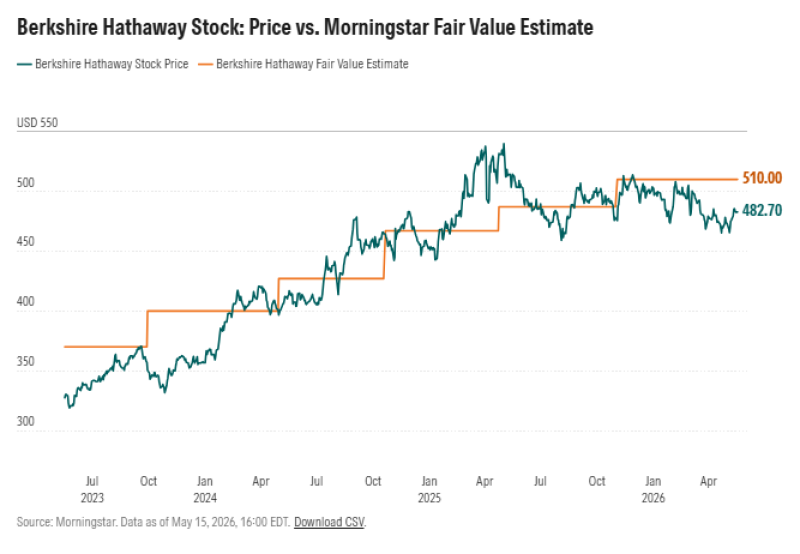

Berkshire Hathaway shares traded around $482.70 in mid-May, compared with Morningstar's fair value estimate of $510, indicating the stock remained modestly below estimated intrinsic value.

Berkshire's own performance helps explain why Buffett's admission matters. The company has built its reputation by allocating capital patiently rather than chasing market trends. Even after recent market volatility, Berkshire's share price has remained close to Morningstar's steadily rising estimate of intrinsic value, reflecting investor confidence in the firm's long-term approach.

Against that backdrop, Buffett's willingness to publicly acknowledge a missed opportunity stands out. Rather than defending every historical decision, he emphasized that identifying a superior business matters more than protecting past judgments.

Greg Abel Takes the Final Decision

Buffett's comments also offered one of the clearest updates yet on Berkshire's leadership transition. While he originated the Alphabet investment, he stressed that Greg Abel now has final authority over investment decisions. Buffett remains closely involved in discussions, but Abel is responsible for deciding whether Berkshire ultimately commits capital.

That distinction provides investors with another indication that Berkshire's succession plan is already operating in practice, while its investment philosophy remains unchanged.

The Broader Takeaway

Buffett's comments are ultimately about discipline rather than regret. Alphabet became one of Berkshire's largest holdings because it met the same requirements Buffett has applied throughout his career: durable competitive advantages, consistently high returns on capital and the ability to reinvest cash flows into future growth.

His admission that Berkshire arrived late does not weaken that philosophy. Instead, it demonstrates that even the most successful long-term investors are prepared to revise their views when the quality of a business becomes impossible to ignore.

Marina Lubimova

Marina Lubimova