Alex Dudov

Alex Dudov

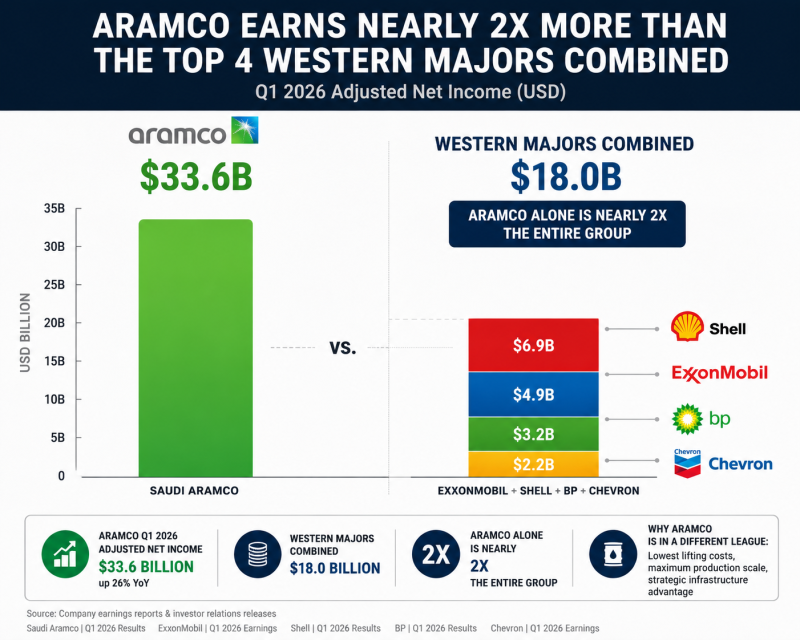

The global energy market may be entering a new era where sheer production scale matters more than almost everything else. Saudi Aramco reported adjusted net income of $33.6 billion in Q1 2026, up 26% year-over-year. That figure is nearly double the combined profits of four Western oil majors during the same period.

Together, ExxonMobil, Chevron Corporation, Shell plc, and BP generated roughly $18 billion in quarterly earnings. Aramco alone produced almost twice as much.

Saudi Aramco generated nearly twice the combined Q1 2026 profit of ExxonMobil, Chevron, Shell, and BP.

The numbers reflect a larger trend quietly transforming global energy economics.

Western oil majors increasingly diversified into renewables, low-carbon initiatives, buybacks, and downstream businesses while facing rising regulatory pressure and higher operating costs. Aramco took a different path: maximize low-cost crude production capacity while investing heavily in strategic infrastructure capable of protecting exports during geopolitical instability.

That strategy may now be paying off at exactly the right moment.

One of the clearest examples is Aramco’s East-West pipeline to Yanbu, which allows Saudi oil exports to bypass the Strait of Hormuz entirely. In a world increasingly shaped by geopolitical fragmentation, shipping disruptions, and energy security concerns, infrastructure resilience itself is becoming a competitive advantage.

The pipeline was built decades ago. Its strategic value may only now be fully understood.

The broader trend extends beyond oil prices alone. Global energy systems are increasingly prioritizing reliability, security of supply, and sovereign control over ideological energy transition narratives. That shift has strengthened producers capable of delivering large-scale supply at extremely low costs during periods of volatility.

Aramco sits almost alone in that category.

Because its lifting costs remain among the lowest in the world, every additional dollar added to crude prices flows disproportionately to the company’s bottom line. While many competitors struggle with capital intensity, refining margins, or transition spending, Aramco’s core business model remains brutally efficient.

The result is a growing divergence between national oil champions and publicly traded Western majors.

That divergence may accelerate if geopolitical tensions around the Middle East, shipping lanes, or global energy security continue intensifying. In such an environment, investors and governments may increasingly reward producers with physical infrastructure advantages rather than companies pursuing diversified energy exposure.

The most important trend may therefore not be the return of Big Oil. It may be the return of geopolitical oil dominance. And right now, Aramco appears to be operating in an entirely different league from the rest of the global energy industry.

Alex Dudov

Alex Dudov