Artem Voloskovets

Artem Voloskovets

the dominant assumption in the housing market has been straightforward: higher mortgage rates would eventually push prices lower.

The first part happened. Mortgage rates climbed to levels not consistently seen since before the financial crisis. Affordability deteriorated, transaction volumes slowed, and buyers became increasingly sensitive to financing costs.

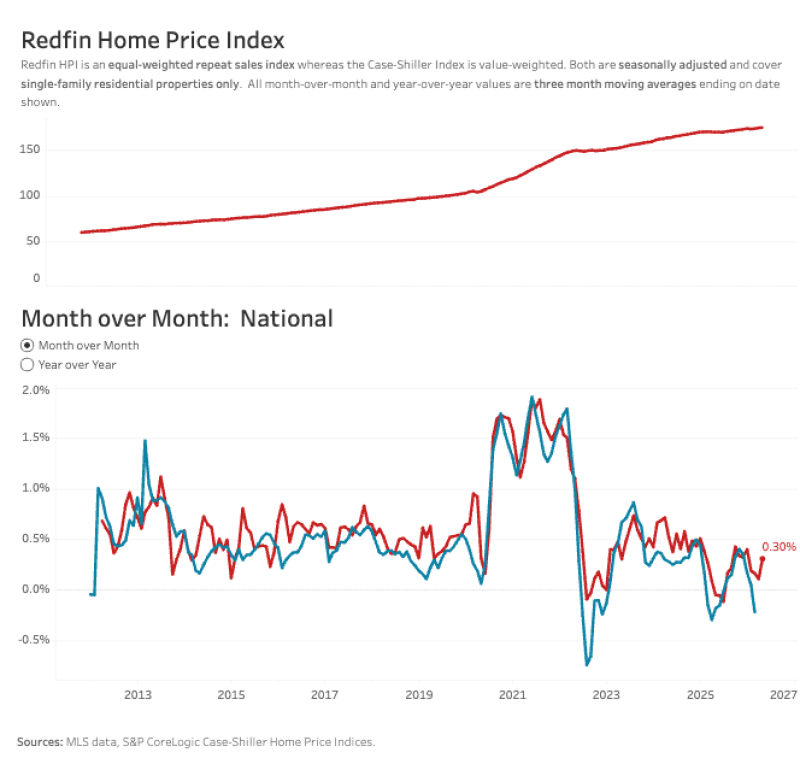

The second part never arrived. According to Redfin, U.S. home prices increased 0.3% in May, the strongest monthly gain since January, and were 2.5% higher than a year earlier. Price growth is no longer rapid, but it remains positive despite borrowing costs that would normally pressure valuations.

Rates Are Restricting Demand

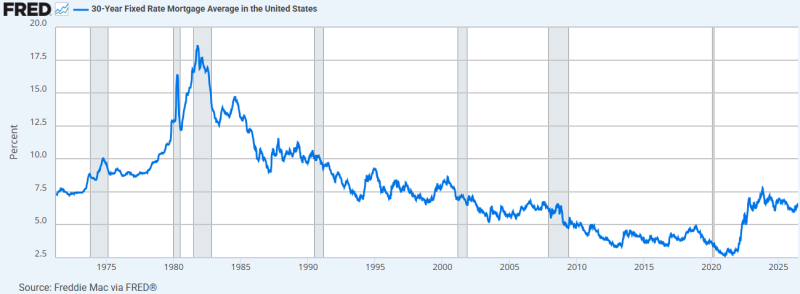

The average 30-year fixed mortgage rate remains near 7%, more than double the levels that prevailed during the pandemic housing boom.

Mortgage rates remain near the highest levels of the past two decades, excluding the inflation shock of the early 1980s. Higher rates have done exactly what monetary tightening is supposed to do. Monthly payments have risen sharply, reducing purchasing power and limiting the pool of qualified buyers.

Housing activity reflects that reality. Existing-home sales remain well below pandemic highs, and demand tends to strengthen only during periods when mortgage rates temporarily retreat. The rate environment is restrictive. The housing market simply faces an even larger constraint.

Prices Continue To Rise

The Redfin Home Price Index shows little evidence of a broad national decline. Home values have continued climbing throughout the rate-hiking cycle, albeit at a much slower pace than during 2021 and early 2022.

Monthly price growth accelerated to 0.3% in May, while remaining well below pandemic-era peaks. The market is no longer characterized by speculative demand or bidding wars across most regions. Instead, prices are advancing gradually because available supply remains insufficient. A market does not require strong demand for prices to rise. It only requires demand to exceed supply.

Inventory Remains Tight

The key housing statistic in 2026 is not mortgage rates. It is inventory. Millions of homeowners hold mortgages originated or refinanced at rates between 2% and 4%. Selling a property often means replacing that financing with a loan carrying a rate near 7%. The result is fewer listings.

Existing homeowners are not just potential sellers; they are also a source of supply. When they stay put, inventory growth remains limited regardless of broader economic conditions. Recent data illustrates the imbalance.

| Metric | May 2026 |

| Existing Home Sales | 4.17 million |

| Monthly Change | +3.2% |

| Inventory | 1.55 million units |

| Months of Supply | 4.5 |

| Median Existing Home Price | $429,300 |

| Housing Affordability Index | 105.6 |

Inventory rose to 1.55 million units in May, yet available supply still represents only 4.5 months of inventory. Historically, a balanced housing market is closer to six months. That difference explains much of the market's resilience. Demand has weakened. Supply has weakened more.

A Market Defined By Scarcity

Housing prices are no longer being driven primarily by cheap credit, as they were during 2020 and 2021. They are being supported by scarcity. Mortgage rates continue to limit affordability and suppress transaction activity. At the same time, the lock-in effect prevents supply from expanding enough to create meaningful downward pressure on prices.

This dynamic changes the way housing data should be interpreted. Weak sales no longer imply falling prices. Higher rates no longer guarantee lower valuations. As long as inventory remains constrained, even modest buyer demand can support price appreciation.

The Constraint That Matters Most

The latest housing data suggests that the market has moved into a different phase of the cycle. The debate is no longer centered on whether mortgage rates are high enough to cool demand. They already have. The more important question is whether enough homes will come onto the market to offset that weakness.

The answer remains no. Home prices continue to rise because the shortage of homes available for sale remains more powerful than the decline in affordability.

Artem Voloskovets

Artem Voloskovets