Marina Lubimova

Marina Lubimova

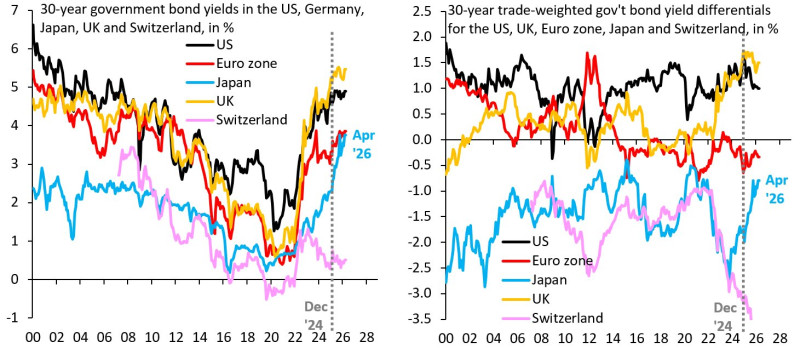

Rising government bond yields have grabbed headlines across major economies - but the more telling signal may lie in what happens when you compare those yields against each other. Economist Robin Brooks has drawn attention to 30-year trade-weighted yield differentials as a sharper lens for spotting where real fiscal pressure is accumulating.

Absolute yields have moved higher everywhere. That's the easy part. What matters is how countries are moving relative to each other.

Why Absolute Bond Yields Are Not Enough

A straightforward look at 30-year government bond yields shows they have risen across the US, Eurozone, Japan, UK, and Switzerland. That broad-based move reflects a global shift in rate expectations rather than stress concentrated in any one economy. When everything goes up together, absolute yield levels lose their diagnostic value - they can't tell you which country is in a tighter spot than its peers.

That's where relative analysis steps in.

The Signal Hidden in 30-Year Bond Differentials

The right panel of Brooks' chart focuses on trade-weighted yield differentials - stripping out the common global trend and isolating how each economy is moving relative to its trading partners. The divergence that emerges is striking:

- The UK shows a strong upward move in differentials

- Japan remains significantly negative

- The Eurozone trends lower

- The US remains comparatively stable

Markets are starting to price long-term risk very differently across countries - and the differential chart is where that story becomes visible.

These relative shifts reflect differences in how markets are pricing long-term fiscal risk - not just rates, but structural confidence in each country's trajectory.

Where Bond Market Pressure Is Building

The chart points to three main areas of concern. The UK's rising differential signals increasing relative pressure - its borrowing costs are moving up faster than the global baseline. Japan sits at the opposite extreme, with a persistently negative differential that reflects deep structural weakness and years of ultra-loose monetary policy creating a distorted baseline. The Eurozone, meanwhile, shows a declining trend - not a crisis, but a steady deterioration in relative terms.

The current structure tells us that markets are beginning to treat these economies as distinct stories - not as pieces of a single global trend.

The US, by contrast, holds a comparatively stable position in differential terms - which is notable given the volume of commentary around American fiscal sustainability concerns.

A Global Bond Market That Is Starting to Differentiate

The takeaway from this framework isn't that yields are rising - that part is well-documented. It's that the global bond market is no longer treating all major economies as part of one synchronized story. Differential analysis cuts through the noise of the broad rate cycle and reveals where genuine divergence is opening up.

For investors and policymakers alike, that divergence is where the real signal lives. Relative positioning - not absolute yield levels - is becoming the more reliable guide to where fiscal conditions are tightening in ways that matter.

Marina Lubimova

Marina Lubimova