Marina Lubimova

Marina Lubimova

The gap between these two indicators suggests the pressure is no longer coming from merchandise trade. Instead, other parts of the balance of payments, including services, investment income, and current transfers, appear to have reduced the overall surplus.

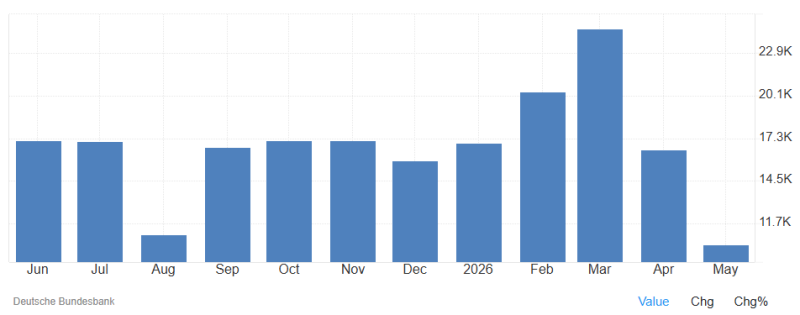

The chart shows the current account surplus rising from around €16–17 billion in late 2025 to more than €20 billion in February and nearly €24 billion in March before falling to roughly €16 billion in April and €10.368 billion in May. The latest reading is the weakest in nine months.

Trade Is Not the Problem

The current account slowdown comes despite continued strength in Germany's export sector. Exports have steadily climbed over the past two years and recently reached new highs, while imports have recovered more gradually. That has allowed Germany to preserve a solid merchandise trade surplus even as global economic growth has slowed.

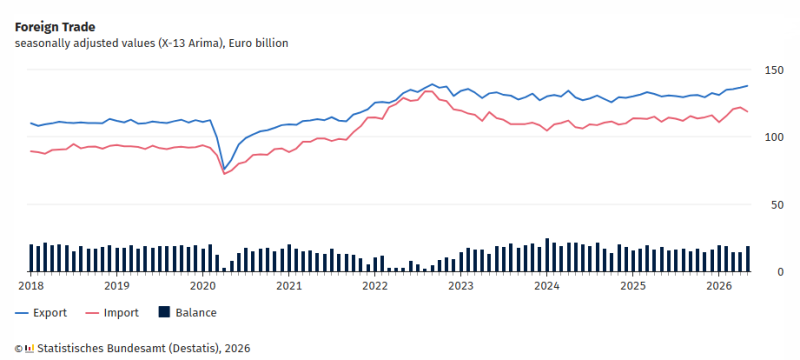

The chart shows exports moving to fresh highs in 2026, with imports following at a lower level. The persistent gap between the two continues to generate a positive trade balance.

The Weakness Lies Outside Goods Trade

A current account balance measures far more than exports and imports of physical goods. It also captures trade in services, cross-border investment income and international transfers.

Because the trade balance remains healthy, May's decline points to weaker contributions from these other categories rather than a deterioration in Germany's manufacturing sector. This distinction is important. Merchandise exports continue to support the economy, but they are no longer enough to prevent the broader external surplus from shrinking.

Germany Is Becoming More Dependent on Exports

The latest figures suggest Germany's external position is becoming less diversified. During periods of exceptionally large current account surpluses, strength came from several sources at once. The latest data indicate that merchandise exports remain resilient, while other external income streams are contributing less than they did earlier in the year.

That leaves the economy increasingly reliant on manufacturing at a time when exporters face slower global demand, higher production costs and growing competition in international markets.

The Next Few Months Will Be Telling

The key question is whether May marks a one-off adjustment after unusually strong readings in February and March or the beginning of a broader trend. If exports continue setting new highs while the current account remains under pressure, investors will likely conclude that the weakness is structural rather than trade-related.

Marina Lubimova

Marina Lubimova