Artem Voloskovets

Artem Voloskovets

Yet the downturn that many economists expected has not materialized. Goldman Sachs recently reduced its estimate of a U.S. recession over the next 12 months from 25% to 15%. The revision matters less than the evidence behind it. Several indicators that typically weaken before a recession are either stable or improving. Taken together, they suggest that economic growth is slowing, but not breaking.

Claims Remain Low

Recessions usually start with a change in employment conditions. Hiring slows, layoffs accelerate, and unemployment begins rising faster than expected. Recent data shows none of that.

Applications for unemployment benefits fell to 226,000. The unemployment rate remains at 4.3%. Employers added 172,000 jobs in May, while average job creation over the last three months stands at 188,000.

Those figures are weaker than the post-pandemic boom, but they remain well above levels typically associated with recession.

Companies Are Still Looking For Workers

Job openings often provide an early signal of how businesses view future demand. When executives become concerned about a downturn, hiring plans are usually reduced before layoffs begin.

The latest data points in the opposite direction. Available positions increased from 6.9 million to 7.6 million, the highest level in nearly a year. That increase suggests employers still expect activity strong enough to justify expanding payrolls.

The Warning Lights Are Not Flashing

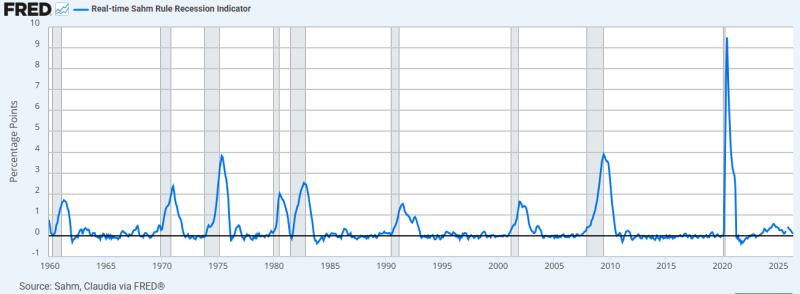

Many recession indicators are designed to identify labor market deterioration before it becomes visible in headline economic reports. The Sahm Rule is one of the most closely watched examples.

Historically, major recessions have been accompanied by sharp spikes in the indicator as unemployment begins rising rapidly. The pattern is visible across downturns in the 1970s, early 1980s, 1990, 2001, 2008, and 2020.

Current readings remain close to the baseline.

The labor market is no longer overheating, but it is not displaying the type of stress that has historically preceded a recession.

Growth Is Slowing, Not Contracting

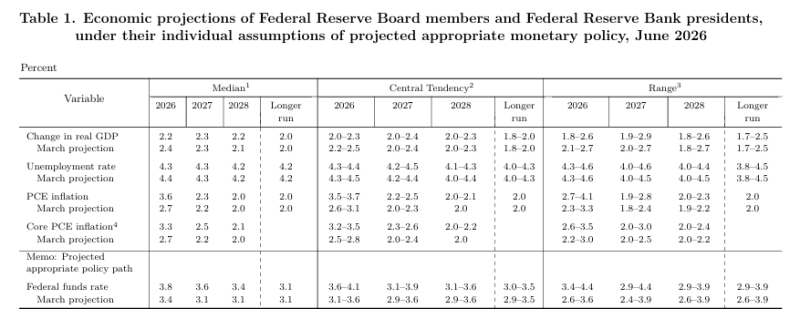

The Federal Reserve's latest projections reinforce the same conclusion. Officials expect real GDP growth of 2.2% in 2026, down from the 2.4% forecast published in March. Inflation expectations moved higher, with PCE inflation projected at 3.6% and core PCE at 3.3%.

Unemployment, however, is expected to remain at 4.3%. The combination is unusual. Growth is moderating while inflation remains elevated. Policymakers are forecasting an economy that continues expanding, but at a less comfortable pace. That is very different from a recession forecast.

Why The Forecast Changed

The reduction in Goldman Sachs' recession estimate did not come from a single data release. It reflects a broader trend visible across employment data, hiring activity, and recession indicators. Layoffs remain limited. Job openings are rising. The Sahm Rule remains subdued. The Federal Reserve still expects positive economic growth.

None of these indicators guarantee that a recession cannot occur. Economic forecasts are frequently disrupted by events that do not appear in the data until much later. What they do suggest is that the balance of evidence has shifted.

A year ago, markets were looking for signs of an approaching downturn. Today, the more difficult question is whether the economy can continue expanding while inflation remains above target. That is a very different problem from the one economists were preparing for.

Artem Voloskovets

Artem Voloskovets