Marina Lubimova

Marina Lubimova

While bullion has captured most investor attention, gold producers are benefiting from a combination rarely seen in previous cycles: historically high prices, constrained global supply and improving financial discipline. The result is expanding profitability that has yet to be fully reflected in mining stocks.

The latest market data suggest investors are beginning to notice.

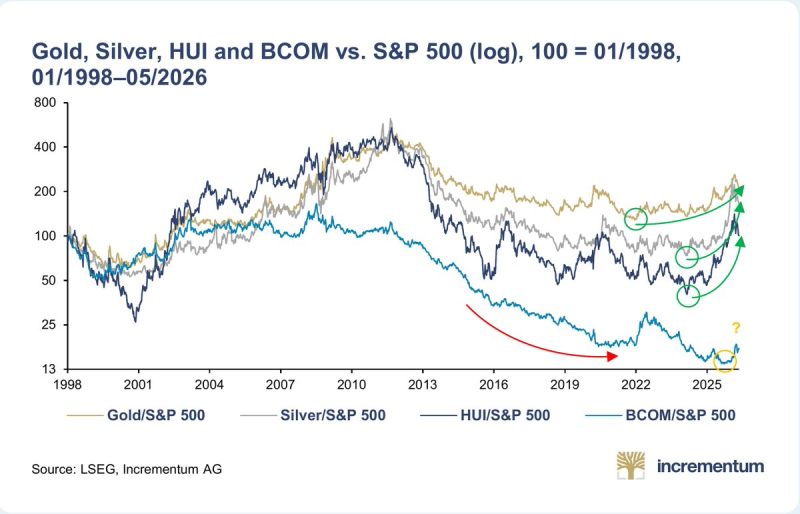

The long-term comparison of gold, silver, the NYSE Arca Gold BUGS Index (HUI) and the Bloomberg Commodity Index (BCOM) against the S&P 500 shows a clear shift in market leadership.

Gold has steadily gained ground versus US equities since 2022, while the HUI index has reversed years of relative underperformance. After spending more than a decade losing ground to the S&P 500, gold-mining shares have begun climbing at a noticeably steeper pace.

Silver is also improving, although from a weaker starting point, while the broader commodity complex remains close to multi-decade lows relative to equities. The divergence suggests investors are becoming more selective. Capital is flowing first toward assets with the strongest exposure to higher gold prices rather than the commodity sector as a whole.

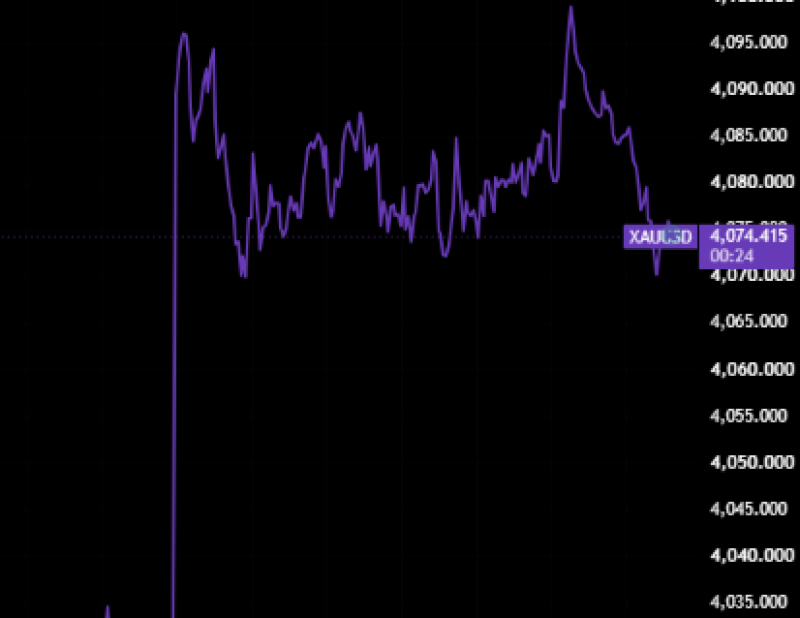

Bullion Has Reached Levels Few Expected

Spot gold recently traded near $4,074 per ounce, extending one of the strongest advances in the metal's modern history.

Unlike previous rallies that were driven by a single catalyst, the current move reflects several overlapping trends. Central banks continue adding gold to reserves, geopolitical tensions remain elevated, government debt has expanded across developed economies, and expectations for lower real interest rates continue to support demand for hard assets.

These conditions have pushed bullion to record territory, creating a pricing environment that dramatically improves mining economics. Every additional increase in the gold price flows directly into revenue, while production changes only gradually.

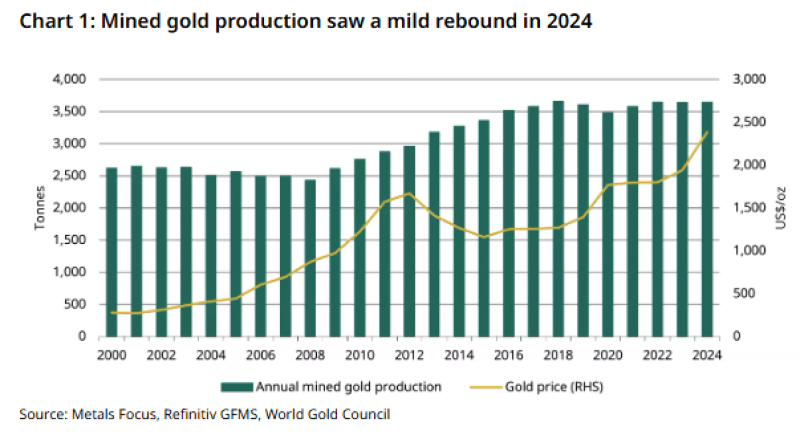

Mine Supply Has Barely Responded

Higher commodity prices normally encourage producers to increase output. Gold has been different.

Global mined production reached roughly 3,645 tonnes in 2024, only slightly above the levels recorded several years earlier. Annual output has remained largely within the 3,400–3,650 tonne range throughout the past decade despite gold prices more than doubling over the same period.

The industry faces constraints that cannot be solved quickly. Large discoveries have become less frequent, ore grades continue to decline and developing a new mine often requires ten years or more of exploration, permitting and construction. Even with stronger prices, producers cannot rapidly bring meaningful new supply to market.

Instead of triggering a production boom, higher prices are being absorbed by an industry operating close to its practical capacity.

Profitability Is Expanding Faster Than Production

Because supply remains relatively fixed, higher bullion prices have a disproportionate impact on operating performance.

Mining costs have increased in recent years as labor, fuel and equipment became more expensive. However, gold prices have risen much faster than operating costs, widening profit margins across the industry.

That improvement is already visible in company results.

Large producers are generating stronger operating cash flow, increasing free cash flow and returning more capital to shareholders through dividends and share repurchases rather than pursuing aggressive expansion projects.

Compared with the previous commodity cycle, balance sheets are healthier and capital allocation has become significantly more disciplined.

Mining Stocks Still Reflect the Previous Cycle

Despite improving fundamentals, gold miners remain far below their previous highs relative to the S&P 500.

The HUI index has recovered sharply from its 2024 lows, but it still trades well below the levels reached during the last major precious-metals bull market. That gap reflects years of investor skepticism toward the sector following weak capital allocation, rising costs and disappointing shareholder returns during the previous decade.

Today's environment looks materially different. Companies are producing similar volumes of gold, selling each ounce at substantially higher prices and generating much stronger cash flows than they were only a few years ago.

If current bullion prices remain elevated, equity valuations may need to adjust to reflect that change in profitability.

The Commodity Rally Has Not Fully Arrived

The same chart also highlights an important distinction. While gold and mining shares have strengthened against US equities, the Bloomberg Commodity Index remains close to historical relative lows. Energy, industrial metals and agricultural commodities have yet to establish a comparable trend.

This suggests the current rotation is centered on precious metals rather than broad-based commodity inflation. Whether that eventually changes will depend on global manufacturing activity, infrastructure investment and overall demand for raw materials.

For now, gold continues to lead the real-assets sector.

A Different Investment Story Is Emerging

Gold itself may no longer be the most interesting part of this cycle. The metal has already reached record prices. Mining companies, however, are only beginning to convert those prices into stronger earnings, higher cash generation and improved shareholder returns.

With global production growing only marginally while bullion trades above $4,000 per ounce, the industry's profitability is improving far faster than its output.

The latest move in mining shares suggests the market is beginning to recognize that shift.

If gold remains near current levels, the next stage of the precious-metals cycle may be driven less by higher bullion prices and more by the companies that produce them.

Marina Lubimova

Marina Lubimova