Artem Voloskovets

Artem Voloskovets

Gold is usually framed as an inflation hedge. That description is becoming outdated. Inflation has eased from its post-pandemic peak, real interest rates remain historically restrictive, and yet gold continues attracting buyers across almost every segment of the market. Central banks are expanding reserves, ETF investors have returned after years of outflows, and private investors are increasing strategic allocations rather than trading short-term price moves. The common denominator is no longer inflation. It is confidence.

Every Financial Asset Depends on Someone Else

- Currencies depend on central banks.

- Government bonds depend on fiscal discipline.

- Bank deposits depend on the banking system.

- Equities depend on future earnings.

- Gold depends on none of them.

It carries no liability, no issuer, no credit risk and no promise that can be broken. For decades, those characteristics made it less attractive than productive financial assets. Today they make it increasingly valuable.

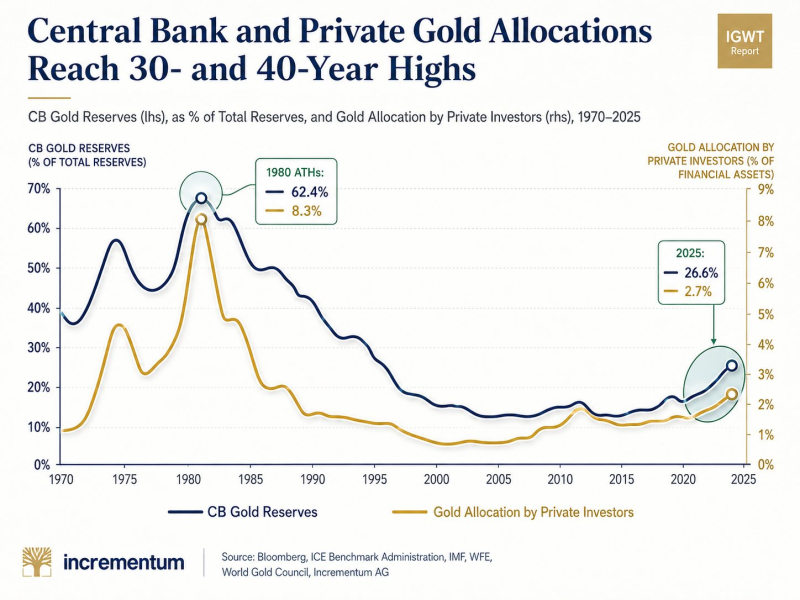

The clearest evidence is not the gold price; it is portfolio allocation. Central banks now keep 26.6% of their foreign reserves in gold, the highest share in more than three decades. Private investors have increased gold holdings to 2.7% of financial assets, the highest allocation in roughly forty years.

The numbers remain well below the inflation-driven extremes of 1980, when allocations reached 62.4% and 8.3%, respectively. The significance lies elsewhere. After forty years of reducing exposure, both public institutions and private capital have reversed direction.

Portfolio allocations change slowly. When they do, they usually reflect changing assumptions about the future rather than short-term market sentiment.

Central Banks Aren't Chasing Returns

Gold generates no income. That has never been the reason central banks own it. Reserve managers are buying an asset that cannot be sanctioned, defaulted on, printed, or tied to another country's balance sheet. As geopolitical fragmentation accelerates and sovereign debt reaches record levels, reserve diversification has become less about maximizing yield and more about minimizing dependence. Gold serves that purpose better than almost any financial asset.

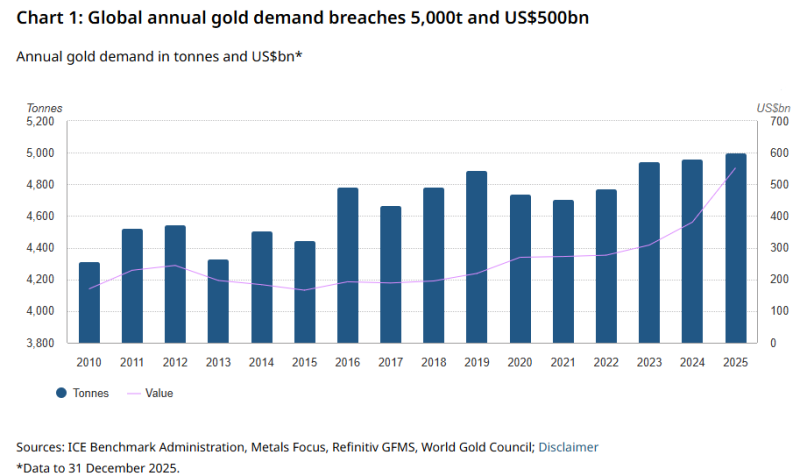

The shift extends well beyond official institutions. Global gold demand surpassed 5,000 tonnes in 2025 for the first time on record, while the market's value exceeded US$550 billion. Those records matter because they combine higher prices with higher physical demand. Normally, expensive commodities discourage additional buying. Gold is doing the opposite. Capital continues flowing into the market despite record valuations, suggesting buyers are responding to strategic considerations rather than price momentum.

The Marginal Buyer Has Changed

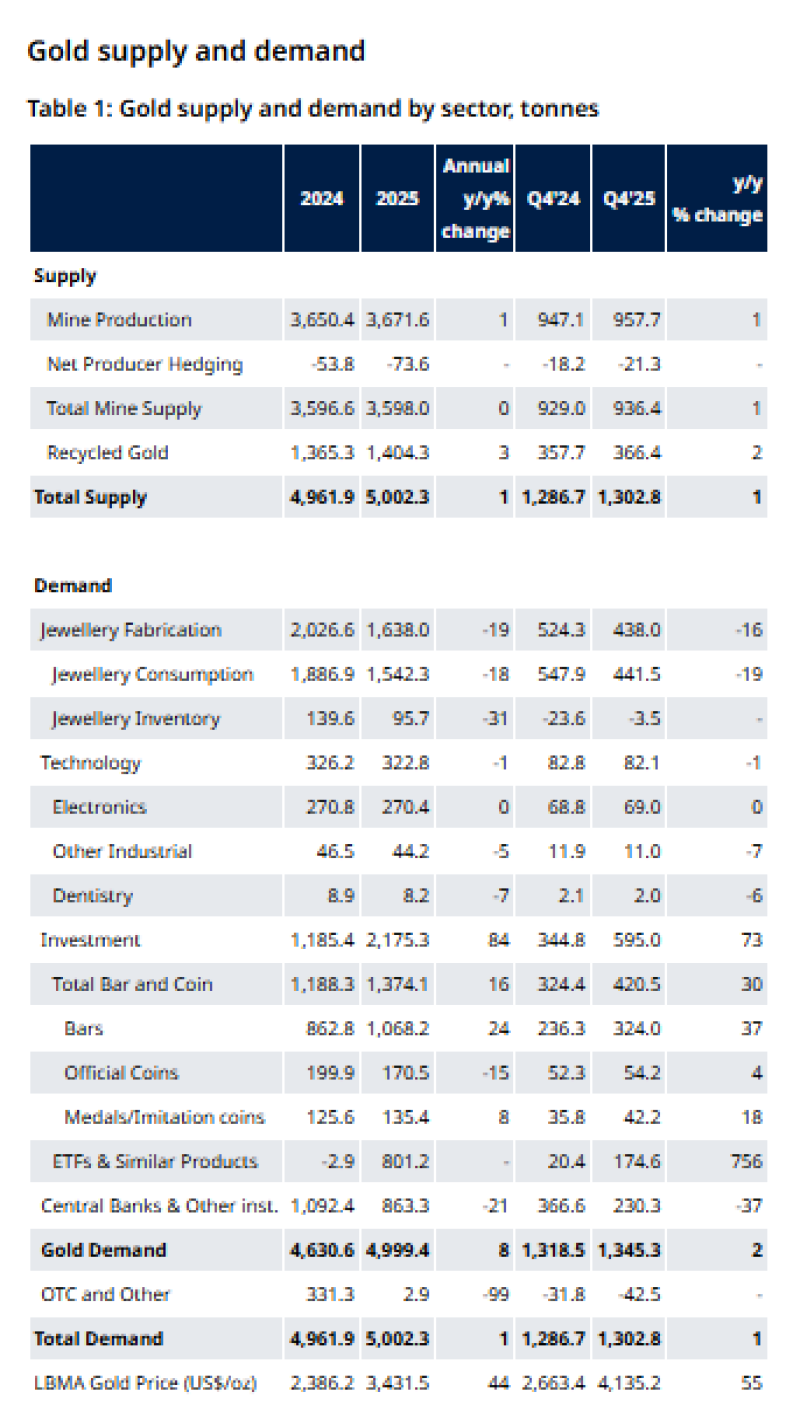

The composition of demand has changed just as dramatically. Investment demand jumped to 2,175 tonnes, an 84% increase from the previous year. ETF products added approximately 801 tonnes, reversing years of weak participation. Demand for bars and coins climbed to 1,374 tonnes, reflecting renewed interest from private investors seeking direct ownership.

Meanwhile, jewelry fabrication fell 19%. Jewelry consumption defined the physical gold market. Today, investment flows increasingly determine marginal demand. That transition changes how the market behaves. Consumer demand tends to weaken when prices rise. Strategic allocation often strengthens instead.

Gold Is Becoming a Portfolio Decision

The current cycle differs from previous bull markets. The rally of the late 1970s reflected inflation. The post-2008 rally reflected monetary expansion. Today's market reflects something broader. Central banks are accumulating reserves.

Institutional investors are rebuilding ETF exposure. Private wealth is increasing long-term allocations. These groups operate independently, yet all are reaching the same conclusion.

Holding more gold reduces dependence on assets whose value ultimately rests on governments, monetary policy, or financial institutions.

The Market Is Repricing Confidence

The defining characteristic of this cycle is not record prices. It is the return of trust-neutral assets. As governments borrow more, geopolitical tensions reshape reserve management, and investors question the durability of the post-Cold War financial order, assets without political or financial counterparties are gaining strategic value.

Gold has not become more productive. The world has become less certain. That distinction explains why demand continues to expand even at record prices and why this cycle may prove more durable than those driven by inflation alone.

Artem Voloskovets

Artem Voloskovets