Marina Lubimova

Marina Lubimova

The company reported second-quarter adjusted earnings of $1.31 per share, above the analyst estimate of $1.28. Revenue reached $12.59 billion, also exceeding expectations. Abbott raised its 2026 adjusted EPS forecast to $5.45–$5.60, from $5.38–$5.58, and maintained its projection for comparable sales growth of 6.5%–7.5%.

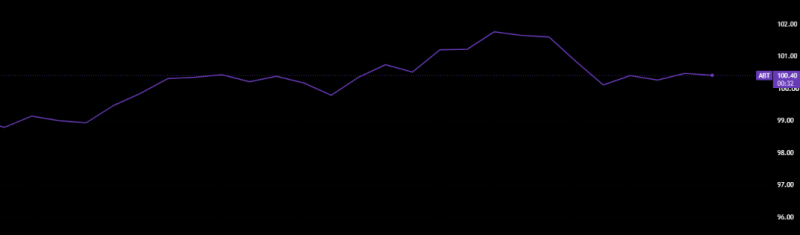

Abbott shares opened near $98.8, climbed steadily and reached an intraday high of about $101.8. The price later retreated to roughly $100.4, giving back part of the initial gain while remaining above the session’s early levels.

The stock chart shows two phases in the market response. Buyers initially pushed Abbott close to $102 as the stronger earnings outlook was priced in. The retreat from the peak suggests some investors used the rally to take profits, but the stock did not return to its starting level. The guidance increase therefore produced a lasting, rather than purely momentary, repricing during the session.

Devices and diagnostics outweigh slower businesses

Diagnostics revenue rose 42% to $3.09 billion, supported by Abbott’s acquisition of Exact Sciences. The deal added cancer-screening products such as Cologuard and Oncotype DX to the company’s portfolio. Cologuard recorded mid-teens growth as testing volumes increased among both new and returning patients.

Cancer screening gives Abbott a more durable source of diagnostics revenue than categories tied to short-lived demand, including COVID-19 testing. It also expands the company’s position in preventive care, where repeat testing and wider screening eligibility can support recurring sales.

Medical-device revenue increased 9% to $5.85 billion, driven by electrophysiology, structural heart products and diabetes care. Sales of continuous glucose-monitoring products, including FreeStyle Libre and Lingo, grew 10.5%.

These businesses are becoming more important to Abbott’s earnings profile. Continuous glucose monitors generate repeat demand, while structural heart and electrophysiology devices benefit from the adoption of less-invasive procedures. Both areas offer stronger growth prospects than Abbott’s more mature product categories.

Nutrition revenue fell 3.1%, reflecting weaker volumes and pricing changes. The decline had a limited impact on the stock because growth in devices and diagnostics more than offset the weakness. Abbott’s performance is now increasingly determined by its technology-based healthcare operations rather than by nutrition alone.

A small forecast change carried a larger signal

The increase in Abbott’s EPS range was limited, particularly at the upper end. The new forecast raised the lower boundary by $0.07 and the upper boundary by $0.02. The share-price reaction indicates that investors interpreted the revision as evidence that Abbott can absorb acquisition costs and weakness in slower divisions without sacrificing annual earnings growth.

The Exact Sciences acquisition had previously created an estimated $0.20 per-share dilution for 2026. Raising guidance while integrating the business suggests that operating performance is offsetting at least part of that pressure.

The maintained sales-growth forecast also matters. Abbott still expects comparable revenue to increase by 6.5%–7.5%, despite weaker nutrition sales and softer conditions in parts of the healthcare market. That outlook depends on continued expansion in medical devices and diagnostics.

Abbott’s valuation case is changing

Abbott has long been valued for diversification and earnings stability. Its current growth mix gives investors another reason to own the stock. A larger share of revenue is now coming from glucose monitoring, cardiovascular devices and cancer testing — markets with recurring demand, higher barriers to entry and stronger structural growth.

The intraday chart captures that reassessment. The stock’s move from approximately $98.8 to a peak near $101.8 shows the initial response to the revised outlook. Its close near $100.4 indicates that some enthusiasm faded, but the market retained part of the gain.

Abbott’s raised guidance was the immediate catalyst. The larger issue is whether its faster-growing healthcare technology businesses can continue to offset weaker divisions and acquisition-related costs. The second-quarter results strengthened that case.

Marina Lubimova

Marina Lubimova