Artem Voloskovets

Artem Voloskovets

The bank continues to rate the stock Buy, signaling confidence in Meta's competitive position while acknowledging that the path to higher earnings has become more expensive.

Rising Costs Are Changing the Valuation

Meta's AI systems continue to improve the company's advertising business. UBS noted that advertising impressions increased 19%, one percentage point higher than the previous quarter, as recommendation algorithms delivered stronger engagement and more effective ad targeting. The bank also expects further improvements in recommendation and advertising technologies over the coming quarters.

Those operational gains, however, are being offset by a rapidly expanding investment program.

UBS cited higher operating expenses and capital expenditure forecasts as the reason for lowering its valuation. The revised assumptions reduced projected 2027 earnings per share by 5% and 2028 EPS by 7%, reflecting expectations that AI infrastructure spending will remain elevated for several years.

The question is no longer whether Meta can build AI infrastructure. Investors are asking how quickly that infrastructure can produce incremental earnings.

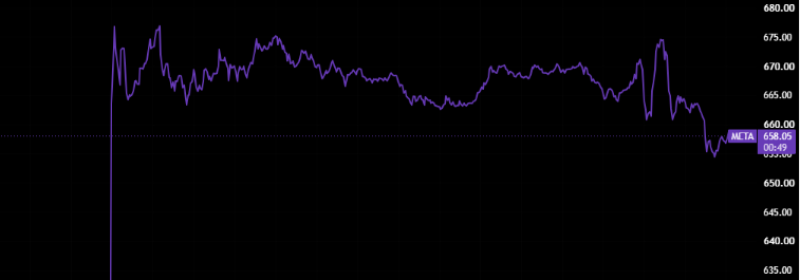

The chart shows Meta trading around $658–660, with shares pulling back from recent highs as investors reassess the balance between AI spending and future profitability.

Revenue Keeps Accelerating

The lower price target comes against a backdrop of exceptionally strong operating results. Meta reported $56.3 billion in first-quarter revenue, exceeding analyst expectations by roughly 2%. Advertising revenue climbed 29% year over year, supported by AI-powered targeting tools and a 12% increase in average ad pricing.

The company's profitability also remains among the strongest in Big Tech. Meta maintains an 82% gross margin, trades at roughly 19x projected 2027 GAAP earnings, and continues to deliver approximately 26% revenue growth, according to InvestingPro. Those figures explain why UBS left its Buy rating unchanged. The business continues to outperform, even as valuation assumptions become more conservative.

Analysts Agree on the Business — Not the Valuation

UBS is part of a broader trend rather than an outlier. Following Meta's latest earnings report, major investment banks adjusted their price targets while largely maintaining positive recommendations.

- Goldman Sachs: $830

- Truist Securities: $840

- Susquehanna: $900

- Evercore ISI: $930

The gap between these targets highlights the uncertainty surrounding AI economics rather than Meta's underlying business. Most analysts expect advertising revenue to remain strong. The disagreement centers on how much value investors should assign to AI projects that have yet to generate meaningful cash flows.

The Market Wants Evidence, Not Promises

For the past two years, technology companies have been rewarded simply for expanding AI capabilities. That phase appears to be ending. Investors are now placing greater emphasis on measurable financial outcomes. Higher capital spending must translate into stronger margins, faster earnings growth, or new sources of revenue.

UBS acknowledged that the financial benefits of Meta's generative AI investments remain difficult to quantify, while the associated operating expenses and capital expenditures are already reflected in financial forecasts. This mismatch explains why valuation multiples are coming under pressure even as revenue continues to grow at a rapid pace.

The range of analyst targets illustrates broad confidence in Meta's long-term prospects, but limited consensus on how quickly AI investments will translate into shareholder value.

A Different Standard for Big Tech

Meta no longer needs to prove it can build advanced AI systems. It has already demonstrated that capability through stronger recommendation algorithms, higher advertising efficiency and sustained revenue growth. The next challenge is financial.

Markets are beginning to judge AI investments by their contribution to earnings rather than by their technological ambition. Until Meta shows that its expanding infrastructure can consistently generate higher cash flow and profitability, analysts are likely to remain cautious about assigning more aggressive valuation multiples. The reduction in UBS's target price reflects that changing standard rather than any deterioration in Meta's business.

Artem Voloskovets

Artem Voloskovets