Marina Lubimova

Marina Lubimova

- Borrowing Is Growing Faster Than Wealth

- Equity Gains Are Creating Their Own Buying Power

- The Shift Appears Clearly In The Balance Sheet

- Institutional Investors Are Following The Same Path

- AI Didn't Create The Rally. It Multiplied It.

- The Risk Isn't The Record. It's The Feedback Loop.

- The Market Is Becoming More Sensitive

- Conclusion

The narrative surrounding U.S. equities has been remarkably consistent. Artificial intelligence is transforming corporate investment, earnings from the largest technology companies continue to exceed expectations, and major equity indices keep setting new highs. Those explanations are all valid. They are also incomplete.

One of the biggest changes in today's market has received surprisingly little attention: an increasing share of equity exposure is no longer financed by fresh capital. It is financed by borrowing.

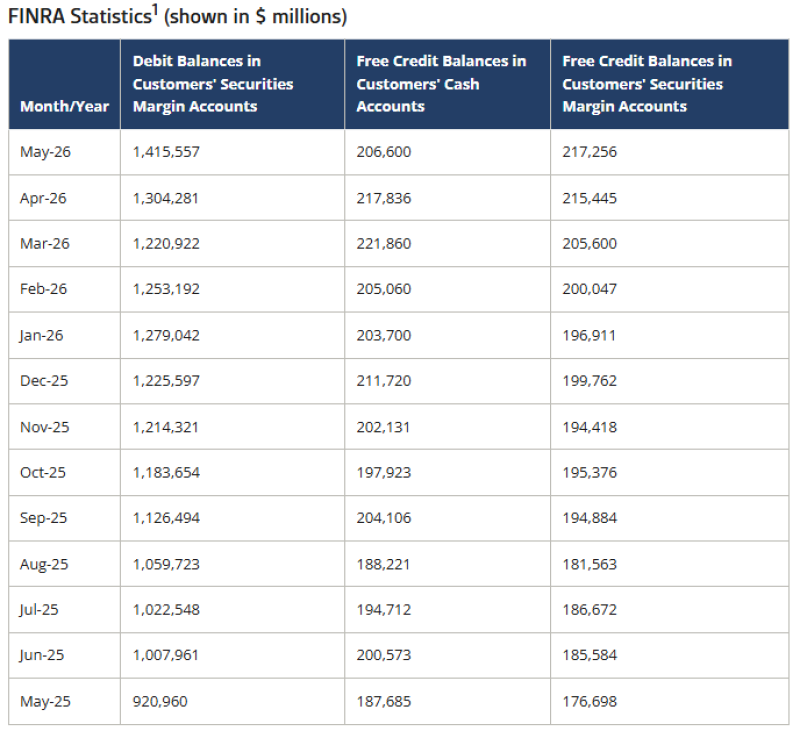

Borrowing Is Growing Faster Than Wealth

FINRA reported that margin debt reached $1.416 trillion in May 2026, the highest level on record. The increase was unusually rapid. Outstanding balances climbed 8.5% in a single month, from $1.304 trillion in April, and were 54% higher than a year earlier, when investors owed $920.96 billion.

The long-term trend is familiar. Margin debt expanded during the dot-com boom, before the Global Financial Crisis and again during the post-pandemic rally. Each cycle reflected rising confidence and higher equity prices.

What makes the current episode different is not simply the new record. Nearly $500 billion of additional leverage has entered the market within twelve months, an expansion rarely seen outside periods of exceptional speculation. The question is not whether investors are optimistic. It is how that optimism is being financed.

Equity Gains Are Creating Their Own Buying Power

Rising markets naturally increase the value of investor portfolios. Higher portfolio values become additional collateral, allowing brokers to extend larger loans against the same assets. Those funds are frequently reinvested into equities, increasing demand and reinforcing the rally.

The process is subtle because it develops gradually. Unlike traditional credit booms, no new wave of bank lending is required. Existing financial assets support progressively larger amounts of borrowing. The result is a market where asset appreciation itself becomes a source of liquidity.

The Shift Appears Clearly In The Balance Sheet

The composition of FINRA's latest statistics tells a more revealing story than the headline number alone. Between May 2025 and May 2026, margin debt increased by almost $495 billion. Over the same period, free cash balances rose from $187.7 billion to $206.6 billion, while free credit balances in margin accounts increased from $176.7 billion to $217.3 billion.

Cash is growing. Borrowing is growing much faster. That divergence suggests investors are relying increasingly on leverage rather than newly committed capital to expand market exposure. The distinction matters because leverage changes how markets react when conditions deteriorate.

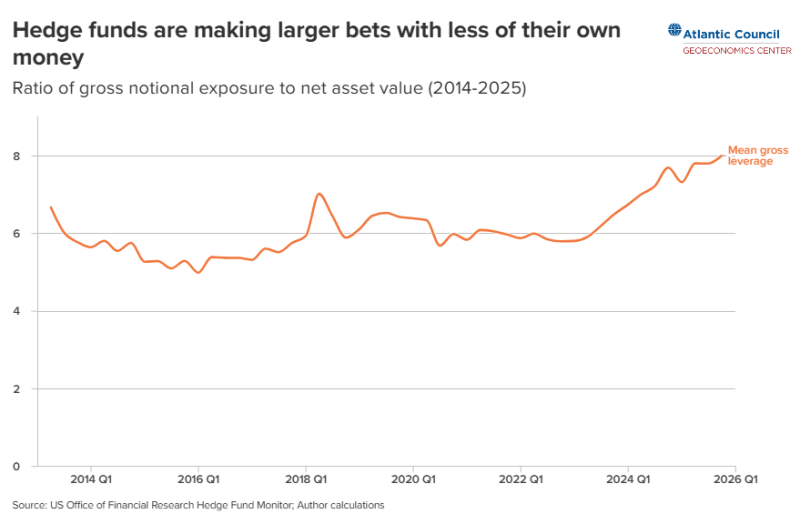

Institutional Investors Are Following The Same Path

Retail investors are not driving this trend alone. Data from the U.S. Office of Financial Research shows hedge fund gross leverage rising steadily over the past decade, increasing from roughly 5× net asset value in 2014 to almost 8× by early 2026.

Professional investors are therefore operating with historically high market exposure at the same time that retail margin borrowing has reached record levels. The overlap is difficult to dismiss as coincidence. Across the market, leverage has become an increasingly common way to generate returns.

AI Didn't Create The Rally. It Multiplied It.

Artificial intelligence explains where capital is flowing. It does not fully explain why market moves have become so powerful.

A small group of companies — NVIDIA, Microsoft, Broadcom, Oracle, AMD and Meta — accounts for a disproportionate share of index performance. As those stocks appreciate, they expand the collateral base supporting leveraged portfolios. That additional borrowing often returns to the same group of companies, reinforcing their leadership.

- The cycle feeds on itself.

- Higher prices increase borrowing capacity.

- Higher borrowing increases demand.

- Higher demand supports even higher prices.

- Artificial intelligence provides the narrative.

- Leverage amplifies the outcome.

The Risk Isn't The Record. It's The Feedback Loop.

Record margin debt has historically accompanied strong equity markets. It is better understood as a consequence of rising prices than as an independent forecasting indicator. The dynamics change once prices begin to fall.

Declining asset values reduce available collateral. Lower collateral forces deleveraging. Forced selling places further pressure on prices, creating a feedback loop that can turn an ordinary correction into a much sharper decline.

Leverage rarely causes market stress on its own. It determines how quickly stress spreads once it appears.

The Market Is Becoming More Sensitive

Strong corporate earnings, substantial investment in artificial intelligence and abundant liquidity support today's equity market. None of those conditions suggests an immediate reversal.

- What has changed is the financial structure beneath the rally.

- More exposure is being financed with debt.

- More institutional capital is operating with elevated leverage.

- More performance is concentrated in a handful of companies.

- Individually, these developments are manageable.

Combined, they leave the market increasingly dependent on stable financing conditions and uninterrupted confidence.

Conclusion

The record $1.416 trillion in margin debt is less important than what it represents. Wall Street is gradually replacing cash with borrowed money. That transition makes rising markets more efficient because leverage accelerates capital deployment. It also makes them less resilient, because every additional dollar of debt increases the need for stable prices. Bull markets rarely end because optimism disappears overnight. More often, they end when the financing behind that optimism becomes difficult to sustain.

Marina Lubimova

Marina Lubimova