Artem Voloskovets

Artem Voloskovets

The performance of Europe's flagship indices increasingly depends on a limited number of companies. When several large constituents come under pressure, the benchmark can weaken even if much of the market remains relatively stable.

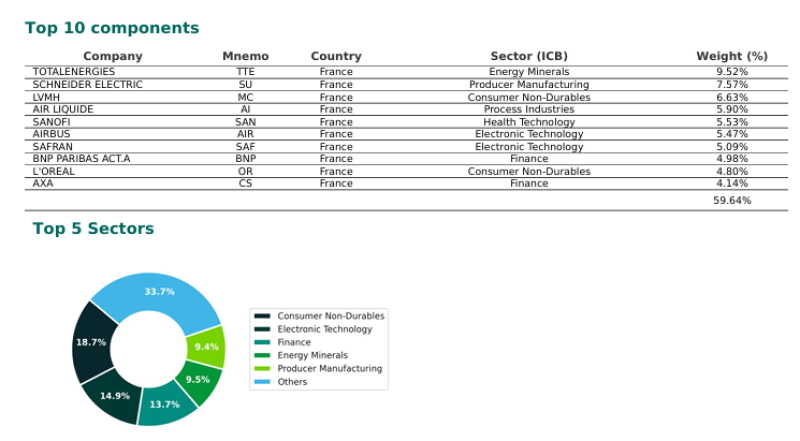

Ten Companies Drive Most of the CAC 40

The CAC 40 contains forty listed companies, but its weight is heavily concentrated at the top.

The ten largest constituents represent 59.64% of the index:

- TotalEnergies — 9.52%

- Schneider Electric — 7.57%

- LVMH — 6.63%

- Air Liquide — 5.90%

- Sanofi — 5.53%

- Airbus — 5.47%

A synchronized decline in only a few of these names is enough to move the entire benchmark, regardless of how the remaining companies perform.

Five Sectors Shape Market Performance

Sector exposure is concentrated in much the same way.

The largest allocations are:

- Consumer Non-Durables — 18.7%

- Electronic Technology — 14.9%

- Finance — 13.7%

- Energy Minerals — 9.5%

- Producer Manufacturing — 9.4%

Together, these industries account for the majority of the index. Market direction therefore depends less on broad economic participation and more on capital flows into a relatively small group of sectors.

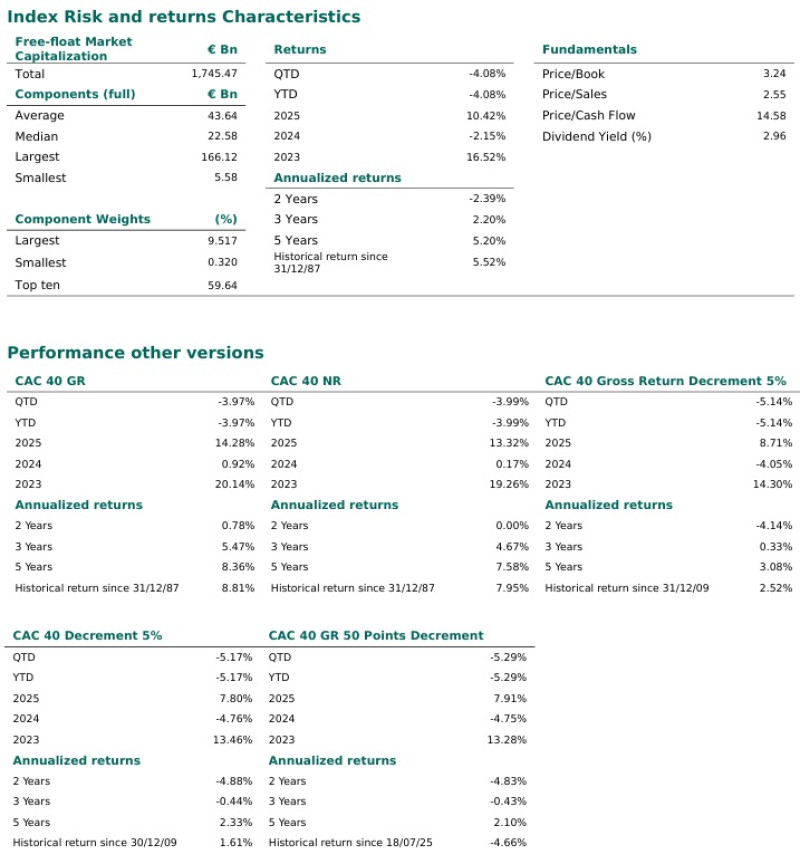

Fundamentals Don't Point to an Overheated Market

Current valuation metrics remain close to long-term norms.

- Price/Earnings — 15.55

- Price/Book — 3.24

- Price/Cash Flow — 14.58

- Dividend Yield — 2.96%

These figures suggest that recent selling was driven more by portfolio positioning than by concerns over excessive valuations.

Recent Returns Show an Uneven Recovery

The market's performance over the past several years explains why investors have become more selective.

- 2023: +16.52%

- 2024: −2.15%

- 2025: +10.42%

- 2026 YTD: −4.08%

Strong gains have repeatedly been followed by periods of consolidation rather than sustained momentum, encouraging investors to reduce exposure during bouts of uncertainty.

Spain Responds Differently

Spain's IBEX 35 declined only 0.34%, outperforming the French benchmark. Its composition differs noticeably from the CAC 40, with greater exposure to banks, utilities and infrastructure companies. Those sectors generally exhibit lower volatility than luxury goods and industrial technology, making the Spanish index somewhat more resilient during periods of cautious market sentiment.

Concentration Has Become the Real Story

Daily index moves rarely explain how a market is changing beneath the surface. The latest session reinforced one structural trend: European equity benchmarks are increasingly driven by a small group of large-cap companies operating in a handful of industries.

For anyone tracking European equities, understanding the composition of an index is becoming just as important as following the macroeconomic events that influence it.

Artem Voloskovets

Artem Voloskovets