Alex Dudov

Alex Dudov

The inflation impact of an oil shock is likely to be short-lived rather than structural. Macro analyst SMQKEr argues that markets are already moving away from sustained inflation fears, pointing to a temporary spike followed by normalization - not a new chapter of persistently high prices.

The market is already shifting away from sustained inflation fears, pointing instead to a temporary surge followed by normalization.

Oil Shock Inflation Spike Into 2026: A Surge That Lacks Staying Power

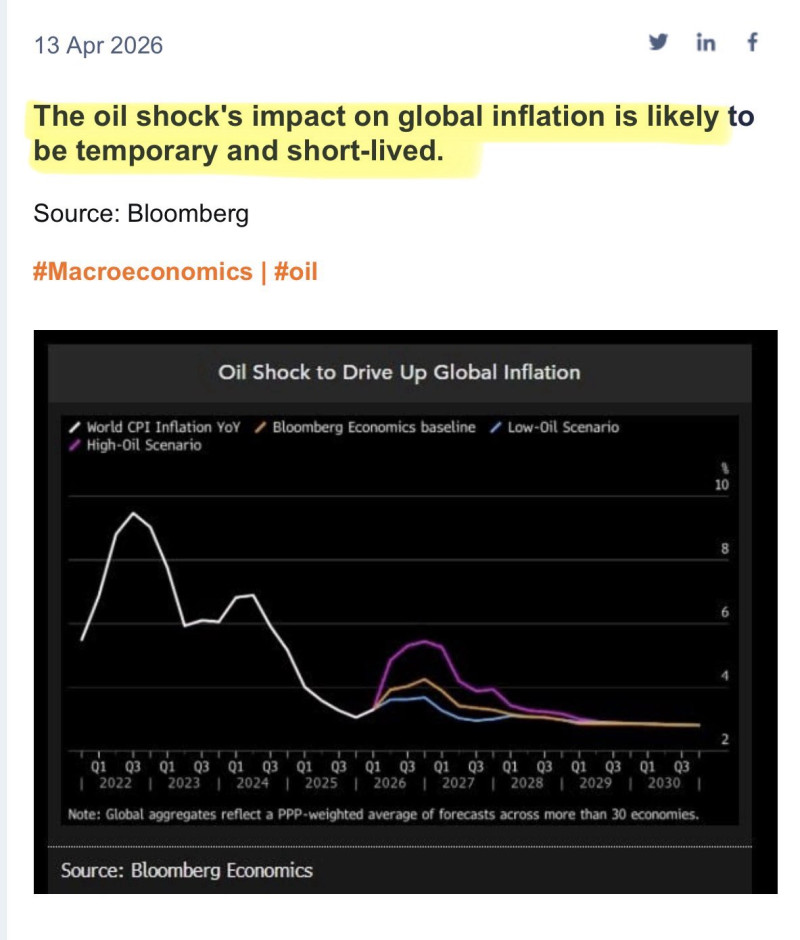

The data shows global inflation reacting to an oil shock across multiple scenarios, with one clear pattern: a spike into 2026, followed by a steady decline. Even in more extreme cases, inflation fails to hold elevated levels for long. This aligns with how energy markets typically behave during supply disruptions. When near-term prices rise faster than long-term expectations, it signals urgency - but not permanence.

In fact, Brent oil backwardation signals near-term supply tightness that historically fades as supply adjusts and demand cools. The structure visible across scenarios reinforces that interpretation: inflation reacts quickly, peaks, and then begins to normalize without forming a prolonged trend higher.

When near-term prices rise faster than long-term expectations, it signals urgency - but not permanence. Backwardation reflects short-term tightness, not a structural shift.

The Oil Shock Market Signal: Pricing a Temporary Event

What stands out is not the magnitude of the oil shock inflation spike, but the inability of the curves to sustain higher levels. The trajectory across all scenarios suggests that markets are not pricing in a long-term inflation regime. This behavior mirrors broader market expectations during recent oil disruptions. Even sharp price increases have been interpreted as temporary dislocations rather than structural shifts, with futures curves and volatility data signaling a short-lived shock.

To put that in perspective, oil's real ceiling may sit near $385,560 when adjusted for money supply - a figure that underscores just how far the current price environment is from any structural inflation threshold. In practical terms, that means inflation driven by oil is being treated as a transient event - one that fades as supply chains stabilize and geopolitical pressures ease.

Beyond Oil Shock: What Drives the Next Inflation Narrative

The analysis also points to a broader transition in market narrative. With oil shock inflation pressures expected to ease, attention may shift toward other catalysts - including regulatory clarity and institutional participation in asset markets. Key shifts to watch include:

- Reduced urgency for central bank rate hikes as inflation normalizes

- Shift in focus from energy-led inflation to structural macro catalysts

- Increased institutional appetite as the inflation risk premium fades

- Geopolitical pressure easing as supply chains rebalance post-shock

Meanwhile, crude oil inventory data adds further context. WTI oil inventories jumped 6.9M barrels to the highest level since June 2024, suggesting that supply is catching up faster than anticipated - a dynamic that historically compresses the inflationary window.

If inflation does not remain elevated, the urgency for further tightening diminishes. That shift is already reflected in expectations around global policy.

As the chart suggests, oil shocks still matter - but their ability to reshape the long-term inflation outlook appears limited. The real signal is not the spike itself, but how quickly it fades.

Alex Dudov

Alex Dudov