Artem Voloskovets

Artem Voloskovets

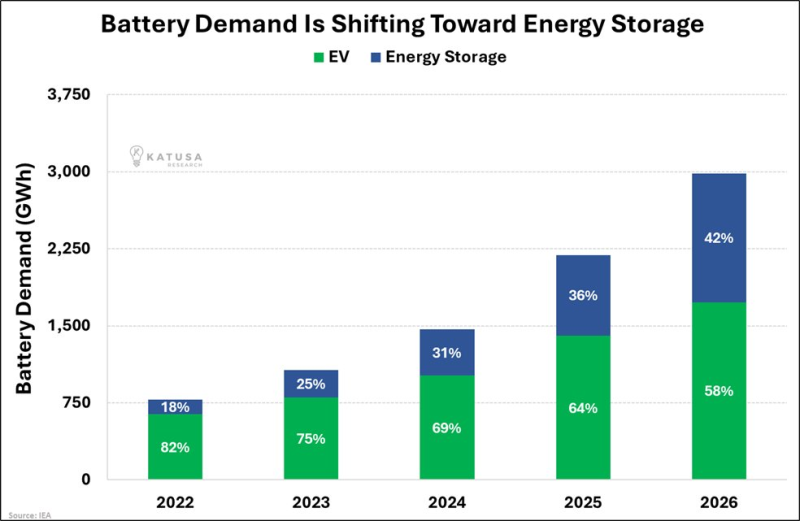

For most of the battery industry's modern history, demand growth came from one place: electric vehicles. Automakers dictated production plans, shaped lithium demand forecasts, and determined where battery manufacturers deployed capital. Energy storage existed, but largely as a secondary market.

That balance is changing. According to IEA data compiled by Katusa Research, energy-storage systems accounted for just 18% of global battery demand in 2022. By 2026, that figure is expected to reach 42%. Over the same period, electric vehicles fall from 82% of battery demand to 58%.

Source: IEA via Katusa Research.

The shift is not the result of weaker EV adoption. Total battery demand continues to rise sharply, from roughly 800 GWh in 2022 to nearly 3,000 GWh by 2026.

What is changing is where incremental demand originates. Grid operators, utilities, renewable developers and industrial power users are becoming major battery buyers alongside automakers. As solar and wind generation expand, storage is increasingly required to balance supply and demand, smooth price volatility and improve grid reliability.

In practical terms, batteries are evolving from a transportation product into a core energy asset.

That transition has important implications for the industry. A market once dominated by consumer vehicle sales is becoming tied to infrastructure spending, utility investment cycles and electricity markets. Battery manufacturers that built their businesses around automakers are finding a second growth engine in grid-scale storage.

- Total battery demand grows from ~800 GWh to ~3,000 GWh (2022–2026)

- Energy-storage share rises from 18% to 42%

- EV share declines from 82% to 58%

- Storage demand expands nearly ninefold in four years

The battery market is not moving beyond EVs. It is becoming larger than EVs alone.

Artem Voloskovets

Artem Voloskovets