Marina Lubimova

Marina Lubimova

The $25 million change is too small to matter on its own. The more relevant signal is that demand for the facility remains close to zero after it once absorbed trillions of dollars in excess liquidity.

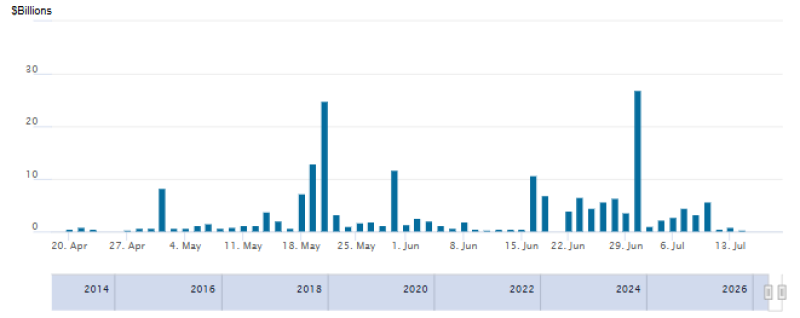

ON RRP usage remained near zero on most trading days, with temporary spikes of approximately $24 billion in May and $26 billion around the end of June.

The supplied chart shows several brief increases, but none developed into a sustained rise. Usage moved above $10 billion on only a handful of days and quickly returned to minimal levels. The pattern points to calendar-driven demand around reporting dates rather than a renewed buildup of idle cash.

The Facility Still Offers 3.50%, but Demand Has Disappeared

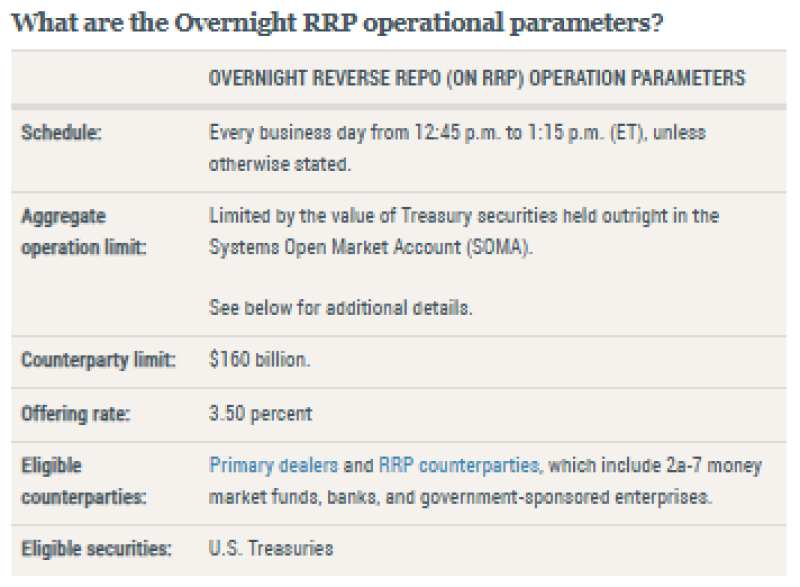

Through the ON RRP facility, approved institutions place cash with the Fed overnight and receive Treasury securities as collateral. Eligible counterparties include primary dealers, banks, money market funds and government-sponsored enterprises.

The current offering rate is 3.50%, while each counterparty may submit up to $160 billion. Operations are conducted every business day from 12:45 p.m. to 1:15 p.m. Eastern Time.

The facility offers a 3.50% overnight rate, accepts U.S. Treasuries as collateral and allows bids of up to $160 billion per counterparty.

The contrast between the $160 billion individual limit and the latest $100 million total shows that capacity is not the issue. Participants are choosing other short-term instruments.

Treasury bills and private repo transactions can offer competitive returns without requiring investors to leave cash at the central bank. Increased bill supply has also given money market funds more options than they had when ON RRP balances were at their peak.

A 20% Drop That Says Very Little

The decline from $125 million to $100 million equals 20%, but percentage changes become misleading when the underlying balance is already negligible. Both operations involved a single counterparty. The movement may therefore reflect one institution adjusting its position rather than a change in system-wide liquidity. The chart provides the more useful context. Daily balances have repeatedly returned to levels close to zero even after short-lived spikes. The facility is no longer serving as a large pool of excess cash.

The Liquidity Signal Has Moved Elsewhere

ON RRP balances were once a closely watched measure of how much surplus liquidity remained in the financial system. That role has weakened as cash migrated into Treasury bills, private repo markets and other short-term assets.

Analysts now need to place greater weight on:

- bank reserve balances;

- the Secured Overnight Financing Rate;

- Treasury bill yields and issuance;

- demand for the Fed’s standing repo facility.

These indicators are more likely to reveal tightening funding conditions than small changes in ON RRP usage.

Daily Operations Continue

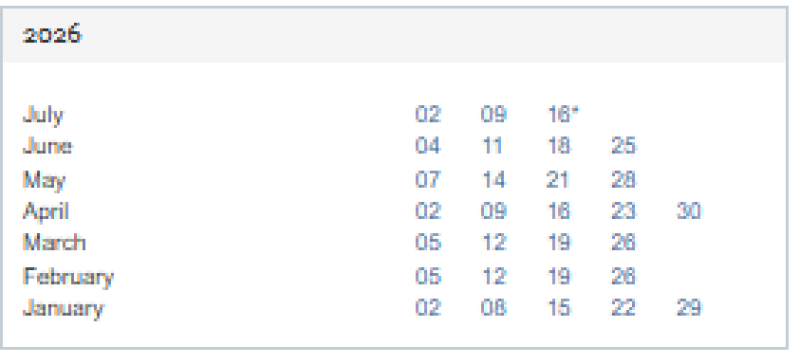

The Fed continues to run the facility on every business day. The supplied 2026 calendar confirms scheduled operations throughout the year, including all listed dates from January through July.

The New York Fed continues to schedule regular ON RRP operations despite the sharp decline in participation.

The latest result does not point to funding stress or a policy shift. It shows that the reverse repo facility has largely finished absorbing the excess cash accumulated during the post-pandemic period. At $100 million, it remains operational but no longer plays a meaningful role as a liquidity reservoir.

Marina Lubimova

Marina Lubimova