Marina Lubimova

Marina Lubimova

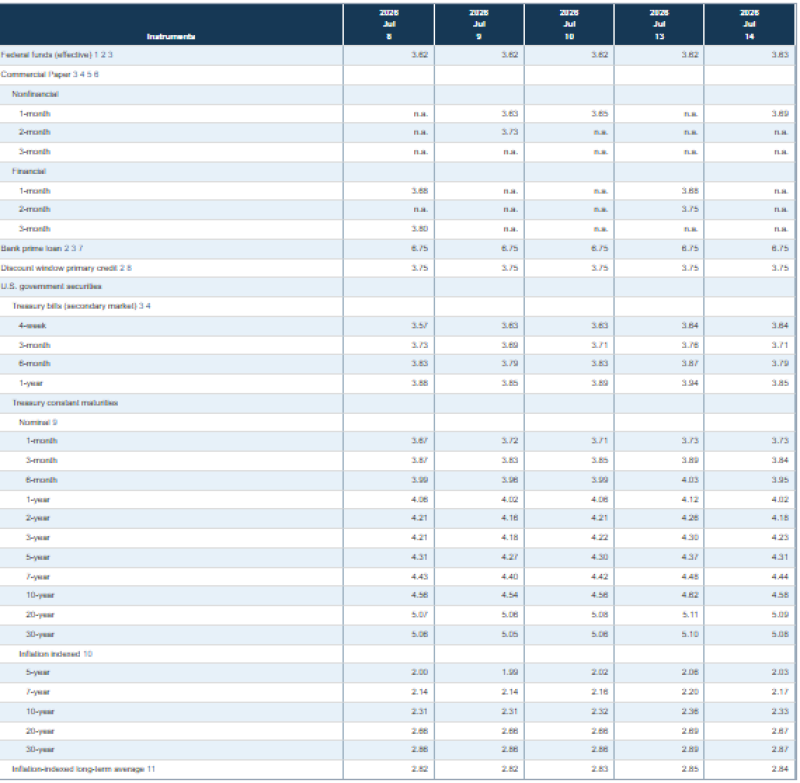

The schedule includes $92 billion of 3-month Treasury bills and $79 billion of 6-month bills on July 20, both settling on July 23. The Treasury will follow with a $13 billion reopening of 20-year bonds on July 22, settling on July 24, before selling $21 billion of 10-year Treasury Inflation-Protected Securities (TIPS) on July 23, with settlement on July 31.

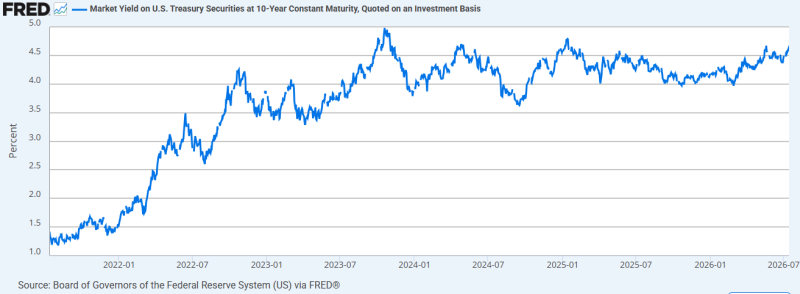

The auctions arrive after a steady increase in long-term yields. Federal Reserve data show the benchmark 10-year Treasury yield climbed from 4.54% on July 9 to 4.58% on July 14, briefly touching 4.62% on July 13. The move has pushed the benchmark close to its highest levels of 2026, reversing much of the decline recorded late last year.

Rising yields typically improve the attractiveness of newly issued Treasuries by offering investors higher income. At the same time, they increase the government's borrowing costs and raise the bar for auction demand, particularly for longer maturities.

Bills Continue to Absorb the Bulk of Treasury Funding

Short-term securities represent $171 billion, or roughly 83% of the week's planned issuance, underscoring the Treasury's continued reliance on bills for day-to-day financing.

Recent trading suggests investors remain comfortable with the front end of the curve. The 3-month Treasury bill yield traded within a narrow range, moving from 3.69% on July 9 to 3.71% on July 14, after briefly reaching 3.76% on July 13.

The 6-month bill yield showed similar stability, fluctuating between 3.85% and 3.89% over the same period.

The limited movement in bill yields indicates that money-market liquidity remains ample despite continued heavy issuance. Strong demand from money-market funds and cash-management investors has so far prevented short-term funding costs from moving materially higher.

Longer Maturities Face Greater Pressure

The week's most closely watched auction is likely to be the reopening of the 20-year Treasury bond.

Unlike Treasury bills, long-dated securities are far more sensitive to expectations for inflation, fiscal deficits and future interest rates. Federal Reserve data show the 20-year Treasury yield increased from 5.07% on July 9 to 5.09% on July 14, remaining above the 5% threshold throughout the week.

Those elevated yields provide investors with some of the highest nominal returns available in years, but they also reflect greater compensation for duration risk. A strong auction would suggest institutional investors are willing to lock in those yields, while weak demand could reinforce upward pressure on long-term borrowing costs.

TIPS Auction Will Gauge Inflation Appetite

The $21 billion sale of 10-year TIPS offers another important test, this time for inflation expectations. Real yields have remained elevated. The 10-year inflation-indexed Treasury yield rose from 2.31% on July 9 to 2.33% on July 14, reaching 2.36% during the week before easing slightly.

Real yields above 2% are historically attractive for long-term investors because they provide positive inflation-adjusted returns even before future CPI indexation is taken into account. That could help support demand for the upcoming TIPS auction despite higher nominal yields elsewhere in the Treasury market.

Auction Results Will Shape the Next Move in Yields

The headline auction sizes are unlikely to surprise investors. Instead, attention will center on the quality of demand.

Markets will focus on bid-to-cover ratios, participation from indirect bidders, and whether auction stop-out yields come above or below prevailing secondary-market levels. Strong demand would indicate that investors remain comfortable financing growing Treasury issuance even as yields approach recent highs.

A weaker reception, particularly for the 20-year reopening, would suggest investors are demanding additional compensation to absorb long-duration government debt, increasing the likelihood that Treasury yields continue their upward trend through the second half of the year.

Marina Lubimova

Marina Lubimova