Artem Voloskovets

Artem Voloskovets

The bond market has stopped behaving as if that outcome is inevitable.

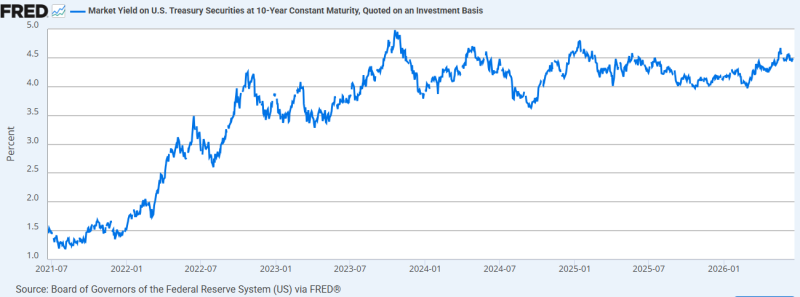

In mid-2021, the U.S. 10-year Treasury yield traded near 1.2%. By late 2022, it had crossed 4%. In October 2023, it briefly approached 5%, the highest level in roughly sixteen years.

The more important observation comes after the peak. Inflation slowed. Expectations for rate cuts increased. Economic growth moderated. Yet yields never returned to the levels that dominated the decade before the pandemic.

The low point of the subsequent decline was roughly 3.6% in 2024. By mid-2026, yields were again near 4.5%. The market has spent three years rejecting the idea that long-term rates belong below 3%.

The Price of Capital Is Moving Higher

Bond yields are often discussed through the lens of monetary policy, but long-term Treasuries are not a direct reflection of the Fed Funds Rate. They represent the market's view of inflation, growth, fiscal conditions, and the return required to lend money for a decade. The persistence of yields above 4% suggests investors are reassessing that required return. Not because inflation remains at 2022 levels. Because the economic environment itself looks different.

A More Capital-Intensive World

Several trends that were once cyclical increasingly appear structural. Governments are running larger deficits. Defense spending is rising across developed economies. Supply chains are being rebuilt closer to home. Industrial policy has returned to the center of economic strategy. Energy systems require substantial investment.

Each trend increases demand for capital. At the same time, governments are issuing more debt to finance these priorities.

For most of the 2010s, debt issuance expanded in an environment of exceptionally low borrowing costs. Today, debt is being financed at yields that are roughly double the average of that period. That changes how investors evaluate risk and how governments evaluate spending.

Valuations Built for a Different Era

The debate around Treasury yields is often framed as a bond-market story. It is not. The reference rate for the global financial system sits at the center of asset valuation. When Treasury yields rise, the present value of future cash flows falls. That affects equities, real estate, venture capital, private equity, infrastructure projects, and corporate investment decisions.

A world built around 1–2% long-term rates produces different valuations than a world built around 4–5%. The adjustment does not happen all at once. It happens through years of repricing.

The Dollar Is Sending a Different Signal

Higher Treasury yields traditionally supported a stronger dollar. That relationship has weakened.

The U.S. 10-year yield has returned to roughly 4.5%, while the Dollar Index remains well below the 114–115 levels reached in 2022. Markets appear increasingly selective about the reason yields are rising.

Yields driven by stronger productivity, investment, or growth tend to attract capital. Yields driven by larger financing needs do not necessarily produce the same currency response. The divergence between rates and the dollar reflects that distinction.

What the Market May Be Accepting

The dominant assumption of the post-2008 period was that low interest rates represented a durable feature of the global economy. The past three years have challenged that assumption. The Treasury market has repeatedly been given opportunities to return to pre-pandemic yield levels and has repeatedly refused.

At a minimum, investors are beginning to price the possibility that the 2010s were the exception rather than the norm. If that assessment proves correct, the significance extends beyond bonds, inflation, or the next Federal Reserve meeting. The defining macroeconomic shift of this decade may be a higher baseline cost of capital. The persistence of 4.5% Treasury yields suggests that adjustment is already underway.

Artem Voloskovets

Artem Voloskovets