Artem Voloskovets

Artem Voloskovets

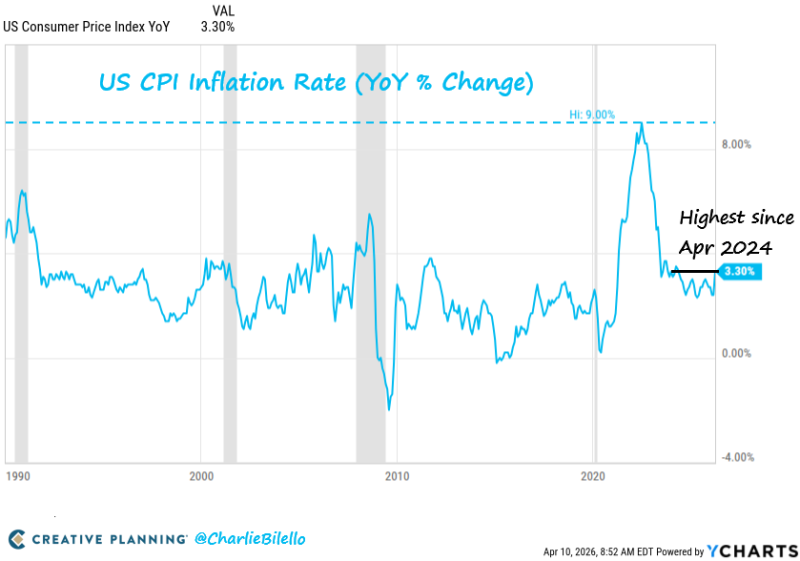

Inflation in the United States is showing renewed firmness, complicating the outlook for Federal Reserve policy. Headline CPI rose to 3.3% in March - the highest level since April 2024 - as Charlie Bilello noted, and the probability of a rate cut this month has dropped to zero.

A Shift Away From the Prior CPI Cooling Phase

The data shows that inflation had been trending lower from its 2022 peak, moving into a more stable range through 2023 and 2024. That downward momentum has now stalled. Instead of continuing lower, CPI has turned slightly upward, reaching 3.3% - breaking the softer pattern that had defined the prior period.

Headline CPI rose to 3.3% in March - the highest level since April 2024 - and the probability of a Fed rate cut this month has dropped to zero.

The 3.3% Level That Reset CPI Expectations

The move to 3.3% is not extreme in historical terms, but it is significant in the current context. This level is now the highest since April 2024, reinforcing that inflation is no longer easing. At the same time, market expectations have adjusted accordingly - the probability of a Federal Reserve rate cut this month has dropped to zero, reflecting how even modest changes in inflation data can reshape policy outlook.

Market expectations have adjusted accordingly. The probability of a Federal Reserve rate cut this month has dropped to zero, reflecting how even modest changes in inflation data can reshape policy outlook.

This alignment between inflation data and rate expectations underscores how sensitive markets remain to CPI developments. This sensitivity is also visible in broader risk pricing - recession probabilities have climbed to around 37% in some models, surpassing earlier benchmarks from major institutions.

Inflation Holding Above the CPI Comfort Zone

The broader pattern suggests inflation is no longer in a clear downtrend. Instead, it is holding above lower levels and showing signs of persistence:

- CPI at 3.3% - the highest since April 2024

- A visible pause in the prior downward trend

- Rate cut expectations reduced to 0% in the near term

Inflation is no longer just declining from prior highs - it is stabilizing at a level that continues to limit the room for policy easing.

This persistence aligns with broader economic signals. Related dynamics are also visible in labor and structural shifts, where changes in employment composition continue to shape the macro environment and inflation behavior.

At this stage, inflation is no longer just declining from prior highs - it is stabilizing at a level that continues to limit the room for policy easing, keeping pressure on both markets and policymakers as they navigate an increasingly uncertain path forward.

Artem Voloskovets

Artem Voloskovets