Artem Voloskovets

Artem Voloskovets

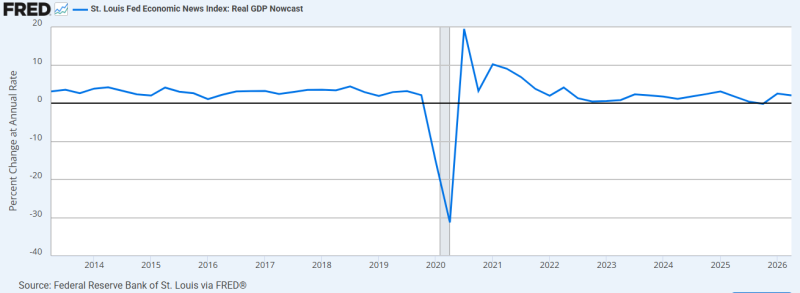

The St. Louis Fed Economic News Index estimated annualized real GDP growth at 2.05753%, close to the economy’s recent trend. The Atlanta Fed’s GDPNow model was more cautious. Its estimate fell from above 4% in May to around 1.7% by mid-July, following a series of downward revisions.

The gap does not point to recession. It shows how uncertain the composition of second-quarter growth remains — and how much the outlook has weakened since the spring.

Growth near 2% remains the baseline

The St. Louis Fed Economic News Index converts incoming economic releases into an estimate of current-quarter GDP growth. Its latest reading places the economy near a 2% annualized pace.

That would be unremarkable by historical standards. Before the pandemic, the index generally fluctuated within a relatively narrow range around low-single-digit growth. The sharpest movements on the chart occurred in 2020, when the estimate plunged below –30% and then rebounded to nearly 18% as the economy closed and reopened.

Since 2022, the series has been far less volatile. Most readings have remained between approximately –1% and 3%. The Q2 2026 estimate of 2.05753% therefore suggests ordinary expansion rather than either a renewed boom or a contraction.

The chart also shows that recent estimates have stayed broadly positive despite intermittent dips below zero. That matters because a 2% nowcast is not simply a recovery from a deeply negative reading. It sits within the range that has characterized the economy for most of the post-pandemic normalization period.

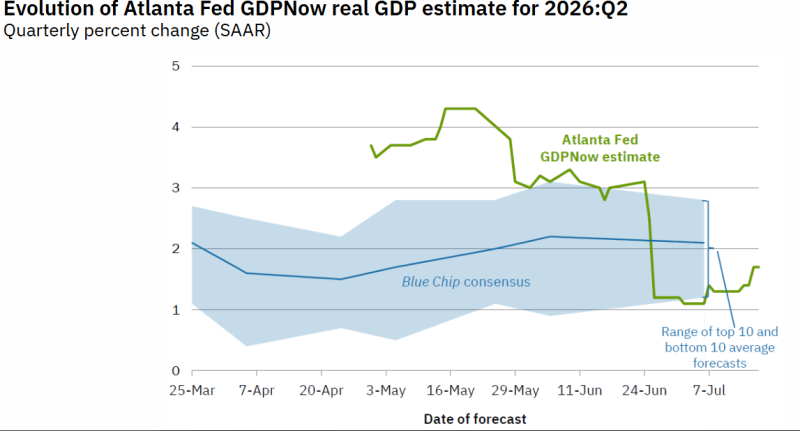

GDPNow’s decline is the more important signal

The Atlanta Fed model changed much more sharply during the quarter. GDPNow began May at approximately 3.5–3.7%, rose to about 4.3% in mid-May, and remained above 3% through much of June. The model then dropped abruptly near the end of June, falling to roughly 1.2%.

It stayed close to that level in early July before recovering to around 1.7% in the latest observation shown on the chart.

The scale of that revision is more informative than the final estimate alone. A decline from 4.3% to 1.7% means the model removed more than half of its expected growth rate over roughly two months.

The shift also brought GDPNow below the Blue Chip consensus. The consensus line remained comparatively stable, moving from about 1.5% in late April to just above 2% by early July. Its forecast range was wide, but the central estimate did not experience the same late-June collapse.

The chart therefore captures two different developments:

- private-sector forecasts gradually moved toward growth near 2%;

- GDPNow moved from an unusually strong estimate to a below-consensus one.

This does not mean economic activity collapsed in June. Nowcasting models can move sharply when new information changes estimates for inventories, trade or other volatile GDP components. Still, the revision weakens the argument that the second quarter delivered another period of rapid expansion.

Recent GDP data have been volatile

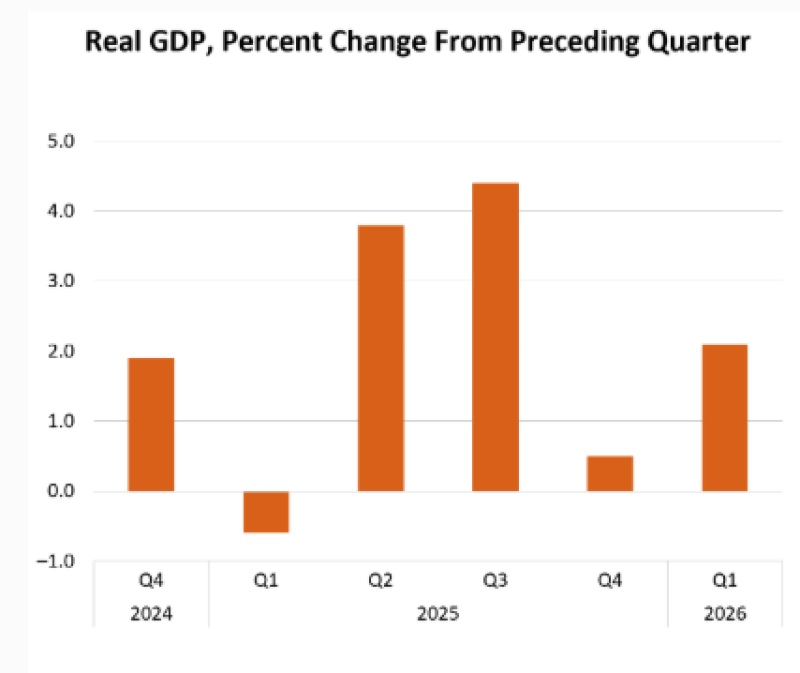

Official figures show that quarterly U.S. growth has shifted sharply since late 2024. Real GDP increased by approximately 1.9% in Q4 2024, then contracted by about 0.5% in Q1 2025. Growth rebounded to roughly 3.8% in Q2 2025 and accelerated to around 4.4% in Q3.

The pace then slowed to about 0.5% in Q4 2025 before recovering to 2.1% in Q1 2026.

This sequence makes a Q2 2026 result near 2% plausible. It would leave growth almost unchanged from the previous quarter and well below the elevated rates recorded in the middle of 2025.

A reading closer to the latest GDPNow estimate of 1.7% would still indicate expansion, but it would also confirm that the economy has settled into a slower phase after last year’s stronger quarters.

Neither model currently signals an outright contraction. The immediate issue for markets is whether growth remains strong enough for the Federal Reserve to keep interest rates restrictive.

A result near the St. Louis Fed estimate would suggest that the economy is absorbing high borrowing costs without a material loss of output. That would give policymakers little reason to accelerate rate cuts unless inflation or employment data deteriorate. A result closer to the lower Atlanta Fed estimate would strengthen the case that monetary restraint is reducing demand. Even then, growth around 1.7% would not by itself justify an emergency response.

The distinction is narrow but relevant. GDP near 2% supports a soft-landing interpretation. Growth moving toward 1% would make the outlook more dependent on consumer spending and labor-market resilience.

The official release will determine which model was closer. Until then, the main conclusion from the available estimates is not that the U.S. economy is approaching recession, but that expectations of exceptionally strong second-quarter growth have largely disappeared.

Artem Voloskovets

Artem Voloskovets