Artem Voloskovets

Artem Voloskovets

- Meta’s stock reflects doubts about AI returns

- External customers would change the economics

- Anthropic is spreading its infrastructure risk

- Spending is rising before the revenue arrives

- A focused compute business, not another AWS

- The contract would test demand, not prove profitability

- Meta’s AI assets may no longer be purely internal

Until now, Meta’s expanding network of data centers, chips and computing clusters has largely supported its own products: advertising systems, recommendation algorithms, generative AI tools and the Llama model family. A contract with Anthropic would show that at least part of this infrastructure can also be sold to external customers.

That distinction matters as Meta raises capital spending and commits hundreds of billions of dollars to large AI data centers. Leasing capacity would not eliminate the cost of that expansion, but it could give the company a direct revenue stream tied to assets that investors currently treat mainly as an expense.

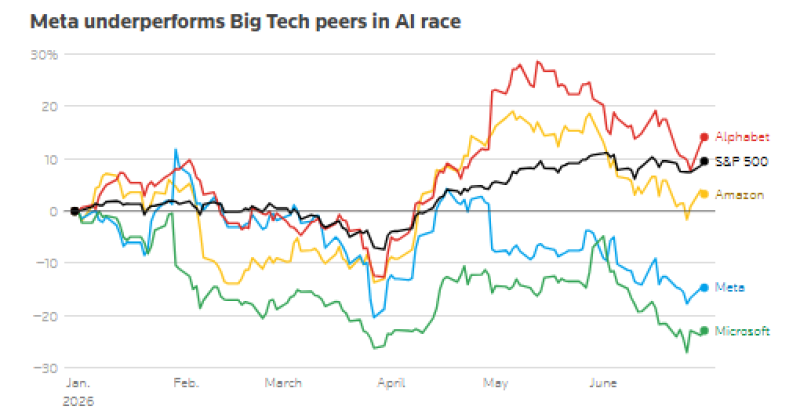

Meta’s stock reflects doubts about AI returns

Meta has spent much of 2026 trailing several large technology companies. The supplied chart shows Alphabet up roughly 13% from the beginning of the year through late June, while the S&P 500 gained close to 9% and Amazon advanced about 5%. Meta fell approximately 15% over the same period. Microsoft performed even worse, declining by more than 20%.

Chart 1. Meta declined by roughly 15% from January through late June 2026, compared with gains of about 13% for Alphabet, 9% for the S&P 500 and 5% for Amazon.

Meta’s relative weakness suggests that larger AI budgets alone are no longer enough to support its valuation. Investors want evidence that the infrastructure will either strengthen the company’s existing earnings or generate revenue beyond its advertising platforms.

A multibillion-dollar Anthropic contract would address the second part of that concern. It would attach a potential customer and commercial value to Meta’s computing buildout.

External customers would change the economics

Meta did not develop its infrastructure as a conventional public cloud. Its systems were built to handle internal workloads across Facebook, Instagram, WhatsApp and the company’s AI research operations.

The proposed Anthropic agreement would extend that role. Meta would remain a major consumer of computing resources while also becoming a supplier to another model developer.

This would allow the company to improve utilization when installed capacity exceeds immediate internal demand. Data centers still carry operating, energy and depreciation costs when portions of their capacity are unused. Leasing that capacity could recover some of those costs without requiring Meta to build a full competitor to Amazon Web Services or Microsoft Azure.

The potential contract would also provide a benchmark for the commercial value of Meta’s AI assets. Investors could begin evaluating the infrastructure using contracted revenue, utilization and margins rather than capital expenditure alone.

Anthropic is spreading its infrastructure risk

A deal between Meta and Anthropic may appear unusual because both companies develop foundation models. In practice, the scale of computing demand is making such alliances increasingly common.

AI laboratories require large and reliable supplies of accelerators, electricity and networking capacity. Depending on one provider can constrain model training schedules and leave a developer exposed to delays or shortages. Anthropic therefore has an incentive to secure capacity from several partners, even when those partners compete with it elsewhere.

The Reuters material provides a comparable example. OpenAI has reportedly planned to add Google Cloud to its computing suppliers despite competing directly with Alphabet in generative AI.

The same logic would apply to Anthropic and Meta. Model competition does not prevent infrastructure cooperation when access to compute becomes more important than strict corporate boundaries.

Spending is rising before the revenue arrives

Meta recently increased the lower end of its annual capital expenditure forecast by $2 billion, bringing the range to $66 billion to $72 billion.

The company has also said it intends to spend hundreds of billions of dollars over time on several large AI data centers. These projects require commitments to land, energy, chips and construction long before they begin contributing to revenue.

Meta is looking beyond its balance sheet to finance part of that expansion. According to the supplied Reuters excerpt, the company sold approximately $2 billion in data center assets as it sought outside partners to help fund the infrastructure required for its AI plans.

The Anthropic negotiations fit that strategy. Asset sales and external financing reduce the amount of capital Meta must commit itself. Compute leases could generate revenue from the completed facilities. Together, these measures would distribute the financial burden of the expansion across partners and customers.

A focused compute business, not another AWS

A computing contract with Anthropic would not immediately make Meta a broad cloud provider. Amazon, Microsoft and Google sell storage, databases, cybersecurity tools and enterprise software alongside raw computing capacity. Meta does not have a comparable commercial cloud ecosystem or an established enterprise sales operation.

Its immediate opportunity is narrower: supplying large AI workloads with specialized infrastructure.

Meta already needs advanced chips and high-speed networks for its own models. Selling access to similar systems could be more practical than building a general-purpose cloud platform from scratch. Demand from well-funded AI laboratories may also be sufficient to support large contracts without thousands of smaller corporate customers.

The model would resemble infrastructure leasing more than a conventional software cloud. Meta would monetize access to scarce computing resources while leaving Anthropic responsible for developing and distributing its models.

The contract would test demand, not prove profitability

The reported $10 billion figure would be substantial, but the economics depend on details that have not been disclosed.

The duration of the agreement, required investment, energy costs, chip mix and minimum usage commitments would determine whether the deal produces attractive returns. A large contract can still carry thin margins when the supplier must construct dedicated facilities or purchase expensive accelerators.

There is also a capacity risk. Meta must ensure that external commitments do not restrict its own model development or advertising operations. Leasing genuinely spare capacity is different from building additional infrastructure specifically for one customer.

Meta’s AI assets may no longer be purely internal

The main significance of the Anthropic talks is not the unusual pairing of two AI competitors. It is the possibility that Meta’s infrastructure is becoming a marketable product.

Meta’s stock decline in 2026 shows that investors remain unconvinced by spending without measurable returns. At the same time, the company has lifted its capital expenditure forecast to $66–72 billion, sold about $2 billion in data center assets and sought outside capital for future facilities.

A long-term compute lease would add the missing commercial component. It would show that Meta can use its infrastructure not only to support its platforms and models, but also to serve customers willing to pay billions for capacity.

The central question would then shift from how much Meta must spend on AI to how much revenue those investments can produce.

Artem Voloskovets

Artem Voloskovets